Abstract

Bioenergy with carbon capture and storage (BECCS) is considered a potential source of net negative carbon emissions and, if deployed at sufficient scale, could help reduce carbon dioxide emissions and concentrations. However, the viability and economic consequences of large-scale BECCS deployment are not fully understood. We use the Global Change Assessment Model (GCAM) integrated assessment model to explore the potential global and regional economic impacts of BECCS. As a negative-emissions technology, BECCS would entail a net subsidy in a policy environment in which carbon emissions are taxed. We show that by mid-century, in a world committed to limiting climate change to 2 °C, carbon tax revenues have peaked and are rapidly approaching the point where climate mitigation is a net burden on general tax revenues. Assuming that the required policy instruments are available to support BECCS deployment, we consider its effects on global trade patterns of fossil fuels, biomass, and agricultural products. We find that in a world committed to limiting climate change to 2 °C, the absence of CCS harms fossil-fuel exporting regions, while the presence of CCS, and BECCS in particular, allows greater continued use and export of fossil fuels. We also explore the relationship between carbon prices, food-crop prices and use of BECCS. We show that the carbon price and biomass and food crop prices are directly related. We also show that BECCS reduces the upward pressure on food crop prices by lowering carbon prices and lowering the total biomass demand in climate change mitigation scenarios. All of this notwithstanding, many challenges, both technical and institutional, remain to be addressed before BECCS can be deployed at scale.

Export citation and abstract BibTeX RIS

Original content from this work may be used under the terms of the Creative Commons Attribution 3.0 licence. Any further distribution of this work must maintain attribution to the author(s) and the title of the work, journal citation and DOI.

Introduction

The latest IPCC Assessment Report (AR5) concludes that achieving climate stabilization at levels consistent with less than 2 °C temperature increase above the pre-industrial level will require sustained greenhouse gas (GHG) emission reductions, leading to near-zero or negative emissions towards the end of this century [1]. Delays in emissions mitigation may mean that human society overshoots or temporarily exceeds its cumulative emissions budget and requires a large use of negative emissions options, defined as the net removal of CO2 from the atmosphere, to bring back cumulative emissions to the desired total. Moreover, increasing the ambition of society's long-term goal (e.g. 1.5 °C target) moves the date after which negative emissions become essential still closer to the present [2].

This has been the subject of numerous papers and assessments (e.g. [3]). Gasser et al [4] find that greater than 1 Gt yr−1 of negative emissions are required to meet the 2 °C target. Scenarios projected by several integrated assessment models (IAMs) show biomass coupled to carbon capture and storage as a key negative-emission technology to achieve cumulative emissions consistent with the 2 °C goal in a cost-effective manner [1, 5]. For example, a comparison study including 15 models [6] concludes that bioenergy with carbon capture and storage (BECCS) could provide temporal mitigation flexibility that reduces near-term mitigation pressure, but they recognize the large uncertainty associated with the viability of large-scale bioenergy deployment. Koelbl et al [7] use the results of the EMF-27 study to explore the long-term role of CCS, showing that models consistently rely on BECCS under stringent climate targets. However, Koelbl et al [7] could not explain the large variation in results across models based on individual model assumptions. Lemoine et al [8] find that the anticipated availability of carbon removal options can reduce the near-term abatement optimally undertaken to meet a stringent climate target. Azar et al [9] use three energy systems models to show that BECCS significantly enhances the possibility of meeting ambitious climate change mitigation targets. Luckow et al [10] find that at carbon prices above $150/tCO2 the vast majority of biomass in the energy system is used in combination with CCS, and that CCS availability reduces the cost of reaching a climate target by offsetting CO2 emissions from sectors that are more expensive to decarbonize, such as transportation. Kemper [11] reviews BECCS applications summarizing recent findings and reporting that 'the majority of current publications seem to agree on a [biomass production] potential of at least 100 EJ yr−1 but are mindful of likely limitations, such as competition for land with food production'.

However, little is known empirically about the global potential of emerging and future negative-emission technologies, the sustainability and cost of large-scale deployment needed to meet proposed climate stabilization targets, or the climate feedbacks of entering a new carbon-negative world. While negative emissions at the scale of a single facility would not be expected to carry significant macroeconomic consequences, negative emissions on a global scale has the potential to change the flow of macroeconomic resources substantially. Although BECCS could allow recovery from an emissions overshoot, the effectiveness of BECCS has not been proven at large scales, and BECCS might never reach technological maturity [12]. Also, BECCS might be seen as a temptation to postpone climate policy action, hindering emissions reductions, since it allows for removing CO2 previously emitted.

In this paper, we use the Global Change Assessment Model (GCAM) to explore the global economic implications of large-scale negative emissions related to bioenergy with CCS in scenarios limiting global temperature rise to 2 °C. We are not considering other net-negative technologies, such as direct air capture, enhanced weathering, ocean disposal, or afforestation (see Smith et al [13] for a review of different negative-emission technologies). Instead, we focus our attention on the magnitude of international financial flows and crop prices that accompany large-scale deployment of BECCS while limiting climate change to 2 °C.

We find that there are major economic implications of deploying BECCS at scales needed to keep cumulative emissions at levels consistent with the 2 °C goal. Global financial flows associated with changed energy and agricultural trade patterns can lead to changes in net trade flows that are a substantial fraction of GDP. Changes in financial flows on this scale will require strong domestic and international institutions for their facilitation. However, there is presently no institutional structure in place that could facilitate the large-scale deployment of BECCS nor manage the large financial flows that would accompany it. Still, no additional technology is needed for BECCS deployment as compared to scenarios using biomass and CCS. Thus, no technological barriers to BECCS deployment exist if CCS is available and large-scale production of biomass is possible. However, BECCS requires specific mechanisms to compensate producers for the CO2 removed from the atmosphere. The millions of tons of CO2 captured would need to be subsidized, or bioenergy producers compensated for the carbon their crops remove from the atmosphere, and the accounting systems must be consistent and deployed internationally.

Methods

We use GCAM—described in detail in the supplemental material—to illustrate the global economic implications of introducing a climate change mitigation policy limiting global temperature rise to approximately 2 °C. In particular, we explore the implication of relying on negative emissions related to bioenergy with CCS by comparing a climate policy scenario where BECCS is available to one where CCS is not available.

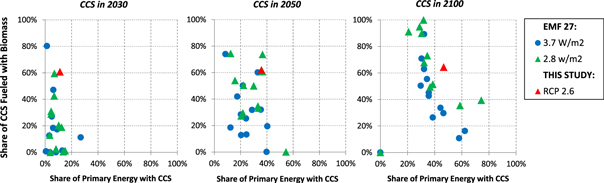

GCAM's use of BECCS technologies in climate change mitigation scenarios occurs predominantly in the electricity and liquid fuels production sectors. In the analysis performed for this study, the projected deployment of CCS technologies—and in particular BECCS—is consistent with the range of other projections reported in the EMF-27 study [14] by 13 IAMs, reported in figure 1. In particular, IA models project a significant share of primary energy with CCS technologies by the end of the century, especially in stringent climate scenarios, with high reliance on BECCS.

Figure 1. Patterns of CCS deployment, with focus on BECCS, in 13 integrated assessment models participating to the EMF-27 study and in GCAM results for the RCP 2.6 scenario, stabilizing radiative forcing to 2.6 W m−2 (red triangles).

Download figure:

Standard image High-resolution imageThe widespread deployment of BECCS in GCAM projections is based on the assumption that biomass can be used across different sectors, such as power plants and bio-refineries, and traded internationally similarly to fossil resources or grains [15]1 . International biomass trade is growing rapidly. While almost no liquid biofuels or wood pellets were traded in 2000, the world net trade of liquid biofuels amounted to over 100 PJ in 2009 [16], and trade of solid biomass, such as wood pellets, amounted to over 300 PJ in 2010 [17]. Larger quantities of these products have been traded in more recent years and are expected to be traded internationally in the future [16–18].

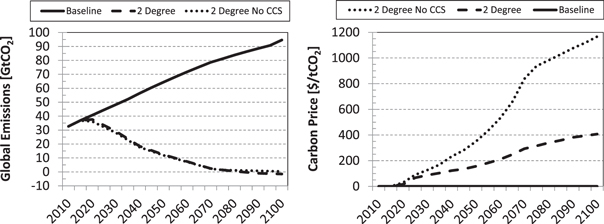

We consider three scenarios in this paper: a Baseline scenario where no climate change mitigation policy is implemented; a '2 Degree' scenario that follows the RCP 2.6 CO2 emission pathway described in van Vuuren et al [19] and largely adopted by the IPCC and the integrated assessment community at large [20]2 ; and a '2 Degree No CCS' scenario that maintains the same cumulative CO2 emissions of the RCP 2.6 scenario, but addresses the lack of CCS (and thus negative emissions from BECCS) by introducing a non-negativity constraint whereby global CO2 emissions can not be net negative3 . Figure 2 shows the global CO2 emission pathways in the three scenarios and the carbon prices generated by GCAM to follow the prescribed emission pathways.

Figure 2. Global CO2 emission (left pane) and related carbon price (right pane) pathways for the three scenarios considered in this paper. Note that the 2 Degree scenario reaches net negative emissions by the end of the century.

Download figure:

Standard image High-resolution imageResults

We observe that the availability of CCS technologies in GCAM reduces the climate change mitigation cost4 by roughly half relative to a scenario without CCS: a reduction equivalent to approximately 4% of global GDP in 2100 in the 2 Degree scenario. In particular, the carbon price needed to reach the climate objective, shown in figure 2, increases by almost three-fold in 2100 if CCS technologies are not available.

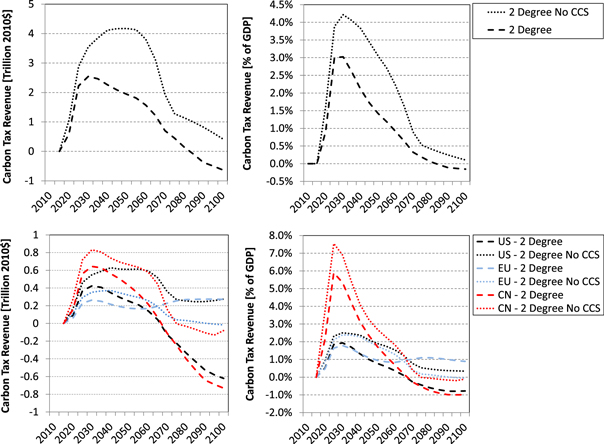

In the 2 Degree scenario, net global CO2 emissions, reported in figure 2, become negative in 2085. At that point, expenditures related to credits for CO2 sequestration become greater than revenues associated with the carbon tax. This has several implications. First, specific mechanisms to compensate biomass producers are required (or in an equivalent system—compensating BECCS deployment). Second, some sort of revenue stream is needed to cover the costs of the mitigation policy (e.g., reallocating revenue from the mitigation policy in previous years which involves recycling over decades and across regions if money collected when CO2 emissions are positive were to be used to pay for carbon removal credits). Finally, international cooperation is required since taxpayers will effectively subsidize biomass producers, who might be located in different regions. If carbon taxes were used to deploy BECCS, global net tax revenues from a climate policy, reported in figure 3, would peak around 2030 at ∼3% of GDP, vanish all together around 2080, and become a burden to governments potentially amounting to a net subsidy of 0.2% of GDP by 2100. Reaching the same climate change mitigation objective without negative emissions (2 Degree No CCS scenario) avoids these issues but increases the burden of the mitigation policy on the global economic activity. That is, the cost of mitigation is higher in a scenario without CCS compared to the scenario in which CCS is available. The revenue from a carbon tax shows significant variation across regions. For example, the availability of CCS increases revenues in US and China, but decreases revenues in the EU, one of the largest biomass exporters in these scenarios.

Figure 3. Global (top panes) and regional (bottom panes) net carbon tax revenues for the two climate change mitigation scenarios in absolute term and as a fraction of GDP.

Download figure:

Standard image High-resolution imageThe results of the scenarios explored here illustrate how the availability of CCS influences the carbon price, and the energy-related financial flows, especially for regions exporting fossil fuels. This confirms the findings of McCollum et al [21], which suggest that carbon pricing reallocates financial flows between importing and exporting regions.

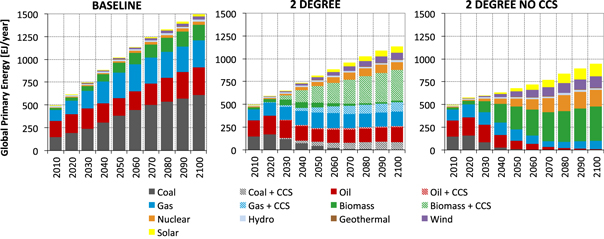

Results from the scenarios explored here show that the introduction of a climate policy likely to maintain climate change below about 2 °C will dramatically shift energy and biomass use and trade. In the 2 Degree scenario primary energy use, shown in figure 4, is considerably reduced compared to the Baseline, as the carbon price leads to increased energy efficiency and reduced demand for final services. Additionally, CCS significantly contributes to the portfolio of technologies deployed: ∼17 Gt CO2 yr−1 are stored using CCS technologies in 2050, primarily for electricity and liquid fuels production, with BECCS accounting for 50% of it. About 31 GtCO2 yr−1 are stored using CCS in 2100, with BECCS responsible for 55%. If CCS is not available the energy reduction is more pronounced (a consequence of higher carbon prices), and renewables, nuclear and biomass take on a larger share of primary energy use, with biomass becoming the dominant energy source by 2100.

Figure 4. Global primary energy consumption for three scenarios.

Download figure:

Standard image High-resolution imageFigure 5 reports the global financial flows associated with fossil fuels, biomass, and agricultural products trade in 2100 for the three scenarios considered in this paper, compared to 2010 historical values. Currently, fossil fuels account for the vast majority of energy trade, accounting for a significant portion of GDP in some major exporting regions such as Middle East and Russia (see figure 11 in the supplemental material). These flows are projected to increase in scale, if no climate change mitigation policy is implemented (second pane in figure 5) as result of increased use of fossil fuels. Also, biomass production in GCAM is projected to increase 8 fold by 2100, absent any climate policy. The imposition of a mitigation policy increases biomass use and reduces fossil fuel use compared to the Baseline scenario; however, the extent of that reduction depends on the availability of CCS. If CCS technologies are available fossil fuel consumption, prices, and trade are reduced compared to the Baseline scenario (see figure 9 in the supplemental material), but not eliminated. If CCS technologies are not available, however, fossil fuels are virtually no longer used by 2100. Thus, while revenues from fossil fuel production would remain significant for exporting regions if CCS technologies are available (third pane in figure 5), they would virtually disappear if CCS technologies were not available (fourth pane in figure 5). For example, as shown in figure 11 in the supplemental material, while international trade of fossil fuel—which accounts for about 35% of the Middle East GDP in 2010—continues to grow in the 2 Degree scenario in absolute terms, its share of GDP decreases. If CCS technologies are not available, the import of biomass in the Middle East overcomes the financial revenues derived from the export of fossil fuels. Revenues from biomass trade are projected to become a significant share of GDP in regions such as the east part of the European Union (∼13%), Australia and New Zealand (∼8%), Canada (∼6%), and South Africa (∼15%) as shown in figure 11 in the supplemental material. If CCS technologies are not available this effect is amplified and extended to other regions (∼19% for the east part of the European Union, ∼16% for Australia, ∼10% for Canada, ∼17% for South Africa, and ∼10% for Russia).

Figure 5. Global fossil fuels, biomass, and agricultural products financial flows in 2010 and in 2100. See figure 9 in the supplemental material for quantity flows.

Download figure:

Standard image High-resolution imageThe export and import of bioenergy is sensitive to assumptions about crop and bioenergy yields and production costs, as well as the availability of CCS. Whether a region specializes in the production of bioenergy or other agricultural and forest products depends on the relative profitability of the various options available to producers. In figure 5, for example, we find that the EU (in particular Eastern European countries such as Poland, Romania, Bulgaria, Hungary, and others) is a major bioenergy net exporter while Latin America is a net importer5 . While one might think that Latin America would be an excellent place to grow bioenergy crops, it is also an excellent place to grow other crops as well. Since land allocation is determined by comparative advantage across crops within a region, more land is devoted to crops with higher relative profit rates. In particular in these scenarios agricultural production, and thus export, of several crops increases significantly in climate change mitigation scenarios in Latin America. This partially compensates for bioenergy displacing other agricultural products in other regions, such as EU. Moreover, a large portion of agricultural products from Latin American is used for the production of first generation biofuels (e.g. sugarcane ethanol in these scenarios). Figure 10, in the supplemental material, shows the land allocation across regions for the different scenarios.

These changes in trade of primary energy commodities have a profound effect on the regional economy, especially for fossil fuel exporting regions, as well as for national energy independence. Figure 6 shows the share of energy traded compared to total domestic energy consumption (negative numbers indicate import), an indicator of the reliance of regions on imported energy. Again, unavailability of CCS technologies affects current energy exporters (regions exporting fossil fuels) by reducing their net energy exports, and favors those regions that produce and export biomass, such us the eastern part of the European Union.

Figure 6. Global net trade of fossil fuel and biomass energy as fraction of domestic consumption by GCAM region in 2010 and in 2100. 100% includes 100 and above.

Download figure:

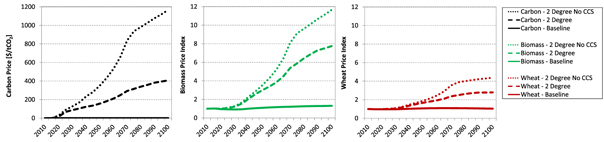

Standard image High-resolution imageThe increased use of biomass due to the climate change mitigation policies leads to a greater competition for the use of arable land, putting significant pressure on the price of various food products6 . Carbon prices influence both the energy and agricultural prices because these markets are closely coupled. The carbon price affects the marginal price for energy by introducing a wedge between the production and sale price of fossil fuels. As the sale price of fossil fuels rises, demand for the untaxed bioenergy increases resulting in higher production and higher bioenergy prices. The higher price of bioenergy results in increases in the prices of other agricultural commodities, as the competition for land puts upward pressure on food prices until those options become equally profitable. As Calvin et al have demonstrated, upward pressure on food prices is removed only when the use of purpose-grown biomass cannot be deployed at scale [22]7 .

Similar results are reported by Klein et al [23], which suggest that the ability of bioenergy to provide negative emissions gives rise to a strong nexus between biomass prices and carbon prices, since the carbon value of biomass tends to exceed its pure energy value. Therefore, Klein et al [23] identify the revenues generated from negative emissions, rather than from energy production, as the primary driving factor behind investments into bioenergy. However, our results show that the nexus between carbon price and biomass price applies in scenarios without BECCS as well, as shown by biomass price reported in figure 7. With higher carbon prices there is an increasing incentive to replace fossil fuels with bioenergy. The dependence of bioenergy prices on carbon prices is stronger in scenarios with CCS (as reported by Klein et al [23] and shown in figure 12 in the supplemental material), due to the potential revenues from net negative emissions, but in scenarios without CCS, still higher carbon prices required to mitigate climate change lead to even higher biomass prices. Under both climate change mitigation scenarios there are significant opportunities for revenues for bioenergy producers. We observe that deployment of CCS, including BECCS, would soften the impact on agricultural price increases, as shown in figure 7. This result is due to the lower carbon prices found in the scenario with CCS. At equivalent carbon prices, the availability of BECCS results in higher food prices.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

Figure 7. Carbon, biomass, and wheat prices.

Download figure:

Standard image High-resolution image{kind=link}

Lotze-Campen et al [24] compare the impacts of increasing cellulosic biomass consumption to 100EJ by 2050 on food prices across different models, showing results consistent with the baseline scenario considered here (where global biomass consumption in 2050 incidentally is 100EJ). Havlík et al [25] use the GLOBIOM model to study the effect of second generation biofuels (e.g., ethanol and methanol produced from cellulosic biomass) showing strong effects on crop prices, and thus potentially on food security, when cellulosic biomass is grown on agricultural land. However, second generation biofuels sourced from forests are shown to have negligible effect on crop prices [25]. In our scenarios biomass displaces mainly pasture, forest and other arable land currently allocated to crop production.

Discussion and conclusions

The availability of CCS, and BECCS in particular, has a substantial effect on the carbon price required to mitigate climate change, and therefore on associated revenues available to governments. While carbon tax revenues inevitably go through an increase and decline pattern under a fixed cumulative emissions budget, net tax revenues are substantially lower with BECCS available because BECCS activities need to be subsidized. When total net emissions reach zero, subsidies and revenues match exactly. Furthermore, net negative emissions for the economy as a whole indicates that the climate change mitigation program is a net cost to the governments, and other revenue sources (e.g., from non-climate sources) are needed to pay for the negative emissions. While these extreme effects only occur after the middle of the century in scenarios likely to limit climate change to 2 °C, tax revenues as a fraction of GDP peak much sooner—in the 2030 timeframe. We observed little effect of BECCS on the global timing of peak tax revenues, which is primarily determined by the emissions path, but we noted significant regional effects, driven by land availability and use.

In addition to changing the flow of carbon tax revenue in an economy, CCS also affects net energy trade. Limiting climate change to 2 °C reduces fossil fuel use. However, CCS tends to temper the decline in fossil fuel trade both by reducing CO2 emissions when coupled to fossil fuels and offsetting them when coupled to bioenergy (the net negative emissions from BECCS compensate positive emissions from fossil fuels). BECCS effectively enhances the emissions reduction capacity of bioenergy, by capturing and storing the carbon that is typically emitted when biomass is converted in final energy carriers (e.g., electricity or liquid fuels). In other words each joule of bioenergy transformed to a final energy carrier with CCS is up to twice as effective in emissions mitigation as one without CCS. This results in lower carbon prices than a scenario without CCS; the lower carbon prices result in less bioenergy produced and traded than when CCS is unavailable8 . Without CCS energy trade is almost entirely bioenergy trade by 2100: fossil fuel use and therefore trade are effectively extinguished. With CCS, fossil fuels continue to be used over the 21st century, guaranteeing a steady financial flow and energy independence to exporting regions. Over the 21st century the value of net exports of bioenergy can be significant relative to GDP, with a larger impact in the scenario without CCS, because the bioenergy price is higher and more bioenergy is used.

Moreover, the introduction of a carbon price and the large-scale use of bioenergy trigger a response in the land-use and agricultural system that increases revenues from the use of land. In particular, as the carbon price rises, the value of bioenergy rises in lock step since it is a renewable non-emitting energy option. As bioenergy becomes more valuable, the competition for the land puts pressure on the price of all agricultural commodities, including food. The increase in food prices is strongly correlated with carbon prices. Thus, the availability of BECCS tempers the upward pressure on price of agricultural products by reducing carbon prices. When carbon prices are equivalent, the presence of BECCS, however, increases food prices.

Both bioenergy and CCS face challenges in their deployment. Large-scale use of bioenergy, for example, might lead to significant indirect land-use change emissions, and/or interactions with food prices and availability. While we have illustrated the effects of including BECCS and CCS in the portfolio of mitigation options (e.g., lower carbon prices, lower food prices, etc), CCS technologies have not yet been deployed at large scale. Such deployment may require the establishment of institutions and policies to support and regulate their use. Moreover, additional technological challenges may arise with large scale CCS use (e.g., related to capture, transport, and storage of CO2). However, the technological challenges do not appear to be fundamentally changed when CCS is combined with bioenergy compared to other applications. Technological and institutional challenges related to large-scale bio-energy and CCS deployment need to be addressed before scenarios such as the ones presented in this paper could be realized.

In this paper we focused on some of the economic implications of the inclusion of BECCS in a climate change mitigation policy. We have explored the economic impact of scenarios consistent with meeting a 2 °C goal in three domains: the macroeconomic scale of potential government tax revenues or expenditures, the impact on energy trade, and the economic impact on food prices. It is important to note that the inclusion of an emissions limitation alone has a major effect on the global economy in these three domains, regardless of assumptions about BECCS. We find that the presence or absence of BECCS from the portfolio of available technologies produces noticeable differences in net government tax revenue, patterns of energy trade, and food prices. In particular, the exclusion of BECCS results in increased tax revenues, reduced fossil fuel trade, and increased food prices. The carbon price is a major mechanism through which the effects of BECCS availability are realized.

The scenarios in this paper include several key assumptions, including perfect international cooperation on climate change mitigation starting from 2020 (i.e., global homogeneous price on carbon), global availability of advanced low-carbon technologies, and large-scale availability of biomass. Previous work has shown that these assumptions can have implications for the cost and feasibility of reaching the 2 °C goal. While this paper demonstrates that GCAM can generate scenarios consistent with achieving the 2 °C goal without relying on net negative emissions under these assumptions, these scenarios also show significant increases in climate change mitigation costs, and significant reductions in total energy use, as compared to scenarios with BECCS. Realizing transformation pathways consistent with the 2 °C goal remains a major technical and institutional challenge.

Acknowledgments

This research is based on work supported by the Global Technology Strategy Program, a research program at JGCRI. The Pacific Northwest National Laboratory is operated for DOE by Battelle Memorial Institute under contract DE-AC05-76RL01830. The views and opinions expressed in this paper are those of the authors alone.

Footnotes

- 1

- 2

The RCP 2.6 emissions pathway limits radiative forcing to 2.6 W m−2 above pre-industrial values in 2100, which was assessed by the IPCC to be likely (>66% chance) of maintaining global average temperature increase below 2 °C, relative to preindustrial levels [30].

- 3

In the 2 Degree No CCS scenario, the RCP 2.6 CO2 emissions pathway is slightly changed across time to ensure that the cumulative CO2 emissions target is met, but constraining emissions to non-negative values in all years.

- 4

This is calculated as the integral under the marginal abatement cost curve and is equivalent to the change in consumer plus producer surplus relative to a no-mitigation baseline scenario in each year.

- 5

Note that in this figure 1st generation bioenergy crops (e.g., sugar cane, corn, soybeans) are included in the agricultural exports. Bioenergy refers to 2nd generation bioenergy crops, such as switchgrass.

- 6

In GCAM crops demand is relatively inelastic. Increased food prices do not affect food consumption directly, but do result in changes in demand for crops used for feed and 1st generation bioenergy.

- 7

Note that this is not the same thing as banning bioenergy all together. Significant biomass feedstocks are available from crop residues, 1st generation biomass (the source of carbon for producing biofuels is sugar, lipid or starch directly extracted from a plant), and organic waste streams.

- 8

Note that at equivalent carbon prices the scenario with CCS results in higher bioenergy production and use.