Abstract

This paper reviews the state-of-the-art of research on African energy transitions and pinpoints critical questions that require answering to allow science-based policymaking. It both highlights unique elements of energy transitions research in the African context, and explains why these need deeper investigation to enable decisions informed by clear and objective country-specific analysis. In doing so, it pinpoints clear areas of future study that are urgently needed at the country level to enable science-informed policy.

Export citation and abstract BibTeX RIS

Original content from this work may be used under the terms of the Creative Commons Attribution 4.0 license. Any further distribution of this work must maintain attribution to the author(s) and the title of the work, journal citation and DOI.

1. Introduction

The transition to sustainable energy systems is a global imperative, and the so-called 'developing world', including most countries in sub-Saharan Africa (SSA), stand at the forefront of this challenge. The SSA region faces a unique set of circumstances, including a rapidly growing population, limited access to modern energy services, and the necessity to balance economic development and industrialisation with socially and environmentally just transitioning (Mulugetta et al 2022). Unlike countries in the 'Global North', the objective of an 'energy transition' in most African countries is not to mitigate climate change, but to achieve universal access to modern energy services—preferably, if cost-effective, using clean technologies to remain consistent with the Paris Agreement.

Achieving a successful energy transition in SSA therefore requires addressing several key questions, which energy modelling literature has not historically had a large focus on. A recent review showed that the academic literature only counts a few tens of studies that focus on country-level pathways towards decarbonised energy systems in Africa, with most of these studies concentrated in a few countries and most of the continent left fully unstudied (Oyewo et al 2023). In other words, it is simply not yet known what 'energy transition' could even mean in understudied countries such as Niger, the Democratic Republic of the Congo, and Madagascar. This lack of information gives rise to black-and-white debates informed by misguided searches for 'one-size-fits-all' solutions, thus impeding any real science-based decision-making (Sterl et al 2023).

One of the central questions is whether renewable energy sources can serve as the primary driver of increased electrification and energy access in the region. Many SSA countries are blessed with abundant renewable energy resources, such as solar, wind, and hydroelectric power (Sterl 2021a, 2021b). However, realising the full potential of these resources is contingent on overcoming numerous challenges.

One such challenge is the high upfront investment required for renewable energy projects and the associated infrastructure. These investments are essential to generate clean electricity and transport it to end-users (ETC 2021), but heavier upfront costs make the buildout of renewables-based power generation infrastructure particularly susceptible to high costs of capital (Agutu et al 2022, IRENA 2023b). The high investment is then exacerbated by a second challenge: the return on these investments. Returns primarily depend on revenue generated from electricity bills from both households and commercial and industrial (C&I) consumers. However, the low per-capita electricity generation in SSA, coupled with the predominance of low-bill customers, poses financial viability concerns for utilities (PwC Africa Power & Utilities Sector Survey 2015).

Moreover, many SSA utilities are financially strained (Trimble et al 2016, Twesigye 2022), and their survival often depends on a small number of C&I customers. Expanding and strengthening the C&I segment is crucial for these utilities to finance grid maintenance, expansion, and large-scale power generation projects. This dependence on a limited customer base makes the utilities vulnerable to a loss of revenue (e.g. if C&I customers defect), and impedes the improvement of grid reliability and increasing energy access.

In addition to expanding energy access, building out renewables-based energy infrastructure will also depend on the electrification rate of total energy demand. However, given that electrification of historically non-electrified sectors—for instance, the large share of household cooking demand met through 'traditional biomass' (IEA 2022)—cannot happen overnight, there is a need to explore the near-term need for increased use of fossil fuels in sectors such as transport, buildings, and industry, such that the narrative of what constitutes a 'just transition' can be framed correctly.

Lastly, at the larger economy scale, the transition narrative may imply substantial shifts in the resource bases of countries' economies, with various African countries being considerably dependent on the revenues from fossil fuel extraction, and/or planning to become so (Davis et al 2021). Any narrative around 'just transitions' must include discourses on alternative opportunities for these countries which have had little historical opportunity to diversify.

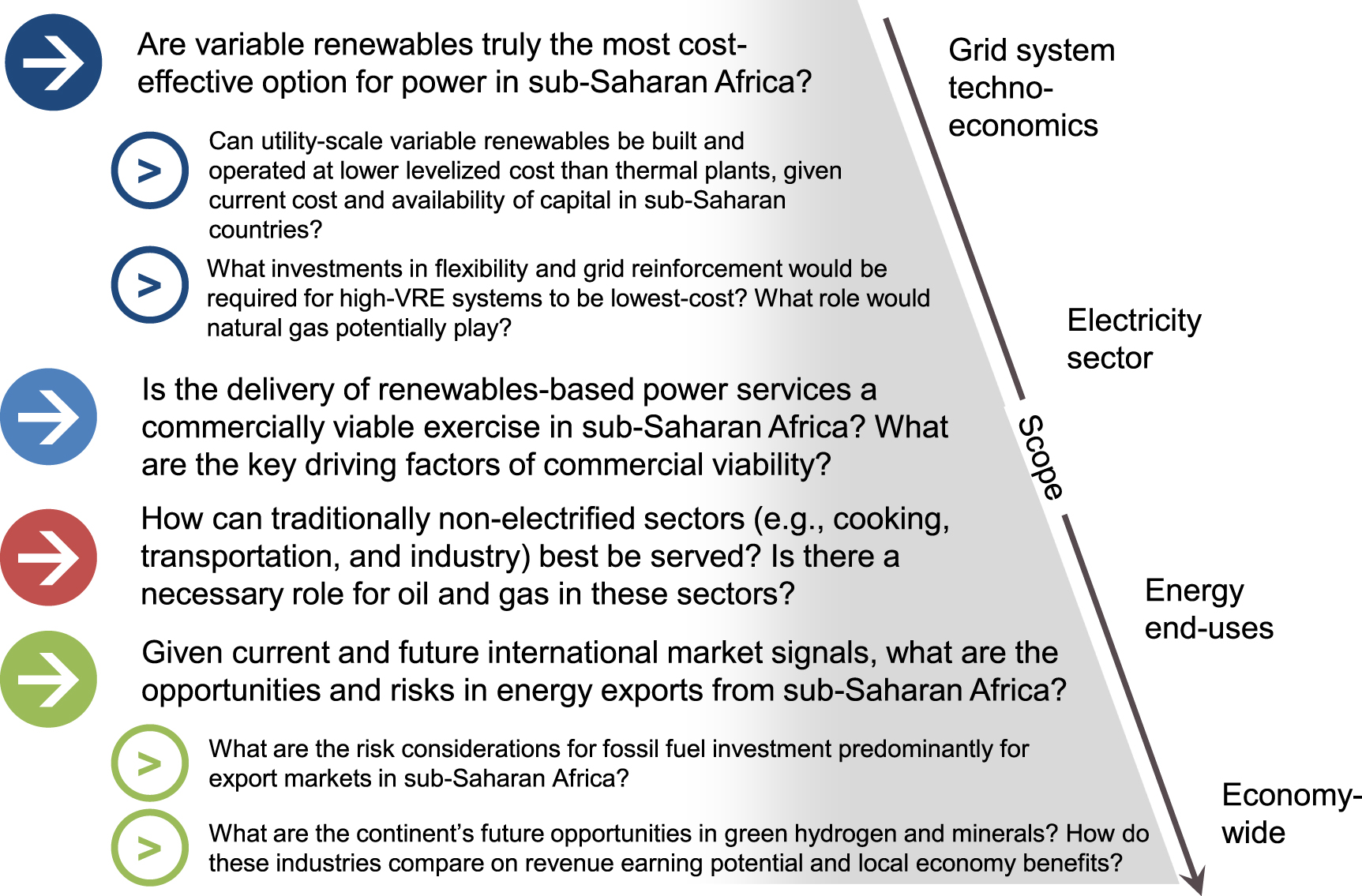

In conclusion, understanding the dynamics of energy demand and supply growth in SSA countries is essential for a successful energy transition (Sterl et al 2023). This involves addressing challenges related to investment, grid reliability, the financial health of utilities, and the wider energy system dynamics of each country, which are summarised in figure 1. This paper explores critical questions concerning the future of energy in SSA, emphasising the need for comprehensive, context-specific analyses to inform sustainable energy policies. The following four sub-sections address the details of each of the four principal questions posed in figure 1 in turn.

Figure 1. Four main areas of questioning which, in the authors' view, are critical to developing perspective on options for African energy transitions. Adapted from (Sterl et al 2023). CC BY 4.0.

Download figure:

Standard image High-resolution image{kind=link}

2. What energy transition means for scaling renewable power generation: are variable renewables truly the most cost-effective option for power in SSA?

SSA benefits from abundant solar irradiation, exceptional wind resources, and extensive available land for renewable power plant installations and other infrastructure. Solar irradiance levels in Africa generally exceed those of other continents, and various regions within SSA offer substantial wind energy potential, with ample land suitable for solar and wind power plants without conflicting with other land uses (Sterl et al 2022). Several countries also boast important hydroelectric power potential, which can play important near-term roles to mitigate solar and wind intermittency (Sterl 2021a, 2021b), although recent research suggests hydropower will rapidly cede in importance towards mid-century (Carlino et al 2023).

Given the resource strength, one would expect variable renewable electricity (VRE) sources, especially solar PV and wind, to be able to provide extremely cheap electricity across many African regions. The cost of electricity from solar and wind power plants, however, is significantly influenced by assumptions regarding the cost of capital (Agutu et al 2022), i.e. the minimum return that prospective investors would expect for providing capital investments. VRE projects, characterised by substantial upfront capital expenditures, minimal ongoing operating costs, and zero fuel expenses, differ notably from fossil fuel-based power plants in their cost structure. Consequently, the sensitivity of the levelised costs of electricity (LCOE) to changes in the cost of capital is heightened for VRE projects compared to fossil fuel-based alternatives (Egli et al 2019, Sweerts et al 2019).

Most energy modelling studies focused on Africa tend to overlook the wide-ranging variations in country-specific Weighted Average Cost of Capital (WACC), at times assuming lower values than reported (IRENA 2021, IEA 2022). Recent surveys and interview-calibrated benchmarking tools have revealed substantial variations in estimated real WACC values across developed and developing countries, ranging from 1% to 20%, where the range from 5% to 20% is exclusively accounted for by developing economies (IRENA 2023b). These findings align with recent scientific research (Agutu et al 2022).

Based on these diverse WACC ranges, the actual LCOE for VRE projects in SSA may significantly exceed that of fossil fuel-based plants in certain countries, despite VRE's proven cost-competitiveness vis-à-vis fossil fuel-based electricity generation in many Global North nations (IRENA 2022). The choice between VRE and conventional power generation options necessitates a careful evaluation of country-specific financial parameters, underscoring the need for tailored energy policies and investment strategies in SSA.

Accelerating the adoption of renewable energy in SSA thus necessitates a robust framework of investment and policies to achieve lower WACC values across a range of markets. Mobilising domestic and international financing for renewable projects, both public and private, coupled with the establishment of favourable regulatory environments, can drive the growth of sustainable power generation (Blended Finance Taskforce 2023).

Another substantial challenge may be posed by the intermittency of VRE. To seamlessly integrate solar and wind power into the electricity mix, it is imperative to develop efficient grid flexibility and energy storage solutions. While battery technologies are advancing, their widespread deployment across SSA requires substantial investments and supportive policies (Oyewo et al 2020, IEA 2022). Additionally, regional cooperation and cross-border electricity trade can optimise resource allocation and enhance grid stability (Sterl et al 2020, 2021). The crucial question here is not whether it is possible to run power grids fully on variable renewables for extended periods of time, as proof from several Global North countries, such as Denmark, Germany and Portugal, has already shown this. However, this proof comes exclusively from countries which already had large-scale, interconnected grids providing 100% access to electricity to start with.

Rather, the question is therefore what investments in grid strengthening, flexibility, and storage solutions would be needed for African countries (with often relatively weak grids as starting point) to be able to use VRE as the backbone of future power system expansion. Much of the research performed to date on SSA capacity expansion appears to have glossed over this question (Oyewo et al 2023), which requires urgent answering. Unlocking the potential of renewables thus demands substantial investments, technological innovation, and tailored policies that align with the unique circumstances of each country (Sterl et al 2023). These unique circumstances must come at the forefront of future research. For instance, certain countries with near-100% shares of hydropower in their electricity mix, like Ethiopia or Guinea, are likely to be relatively readier for absorbing initial shares of VRE than countries without such dispatchable capacity at their disposal, such as Niger or Eritrea (Sterl et al 2021). Similarly, in regions where cross-border interconnections already have a relatively strong buildout (e.g. West Africa), VRE integration may find fewer hurdles than in regions where this is not the case (e.g. Central Africa) (Sterl 2021a, 2021b).

Answering the above question will not only have to consider the technical aspects, but also the financial and market-related ones. Determining how best to structure financing for new interconnectors or storage projects, with what types of financing (foreign direct investment, development finance, climate finance, etc.), and how these projects can be embedded in regional power pools and participate in future electricity markets, is crucial to allow the smooth uptake of more and more VRE (Elabbas et al 2023).

3. What energy transition means for expanding energy access and electrification strategies: what are the key driving factors of commercially viable power delivery?

The expansion of electricity access in SSA is a complex challenge, transcending mere demand projections and technology optimisation, and with substantial implications for economic development, healthcare, education, and overall quality of life. The region lags behind the rest of the world in terms of electrification rates, with over half of its population still lacking access to reliable and modern electricity services (IEA 2022). Addressing this issue requires a holistic approach that encompasses both grid and off-grid solutions, innovative financing mechanisms, and policy reforms.

As of 2023, SSA per-capita electricity generation remains exceptionally low, with estimates hovering around 200 kWh/capita/year. Projections indicate limited growth, reaching 500–700 kWh/capita/year by 2030, even with universal household access (IRENA 2020, IEA 2022). These projections imply that most end-users currently accounting for the high statistics of people without access to electricity, will maintain low electricity consumption levels against a backdrop of a scarcity of C&I customers. The cost of connecting low-consumption households to the grid is a substantial barrier for utilities, as recovery through electricity bills may not occur within viable timeframes (Lee et al 2018).

In both the developed and developing worlds, utilities generally heavily rely on a small number of C&I customers for financial sustainability. If the C&I segment is relatively weak, this constrains their capacity to invest in grid maintenance and expansion. This predicament is exacerbated by the imperative to expand electricity access to non-C&I customers, relatively unique to SSA, and the inherent challenge of low grid reliability, which can potentially deter C&I customers from utilising grid electricity. Financial struggles among SSA utilities are well-documented (Trimble et al 2016, Twesigye 2022), with only one-third able to cover operating and debt-service costs as of 2018, further exacerbated by the COVID-19 pandemic (Balabanyan et al 2021).

Therefore, it is imperative to explore strategies for strengthening the C&I sector across African countries to avoid or escape the utility death spiral. Further, mechanisms must be investigated to foster domestic electricity uptake that align with development objectives without overburdening utilities. What this means in practice is that the supply, the transport, and the offtake of increased electricity generation must come as a 'package deal' in many SSA economies. This is a relatively unique frame that does not apply across, for instance, most Global North countries, where the offtake by large-scale customers is typically guaranteed, and investments in grid infrastructure are typically focused on strengthening existing infrastructure rather than building up a grid from close to 'scratch'.

Here, an important role might exist for mini-grids and standalone systems (Lucas et al 2017, Mentis et al 2017): in the initial stages of grid expansion, such systems—especially when located far from the grid and catering to relatively low demands—can be cost-effective vis-à-vis connecting to a utility-scale grid (Lucas et al 2017). Therefore, developing off-grid systems could be a lever towards providing initial 'bundles' of electricity access to households in the lower tiers (ESMAP & SE4All 2015) until induced demand is high enough for grid expansion to make financial sense. Here, as on the utility-scale evoked above, it is of paramount importance to establish feasible business models for off-grid systems that consider the financial means and willingness-to-pay of its customers, both households and businesses (Bhandari et al 2020).

Again, retaining the viewpoint of uniqueness of each country is paramount. Country-level policy on on-grid versus off-grid electrification may differ markedly; Ghana is an example of a country that has historically insisted on maximising grid buildout as opposed to relying on off-grid solutions (and reaching comparatively high access rates in the process) (Ibrahim et al 2023); whereas Mali, for instance, has a higher share of people using off-grid electricity than people relying on the grid, though also a much lower overall electrification rate than Ghana (Logan and Han 2022).

In conclusion, expanding electricity access in SSA extends beyond demand forecasts and technology optimisation (Sterl et al 2023). Understanding how utilities operate and addressing their financial health is pivotal in determining the pace and extent of electrification. The growth and resilience of the C&I segment across SSA are instrumental in facilitating utility-driven expansions. This demand-centric view is a critical yet understudied aspect of African energy transitions, warranting further investigation at the country-level.

4. What energy transition means for end-use electrification and the role of fossil fuels: how can traditionally non-electrified sectors best be served, and what is the role for oil and gas?

This section delves into the electrification landscape of SSA, highlighting the role of fossil fuels in traditionally non-electrified sectors and the transition toward cleaner alternatives. Non-electrified sectors, including household cooking, transportation, and industry, pose a unique set of challenges. Traditional biomass remains a prevalent cooking fuel, while road transportation relies heavily on diesel and gasoline (IEA 2022). Heavy industry, which in SSA is dominated by cement making, requires fossil fuels for high-temperature processes.

Rapid electrification of these sectors faces hurdles due to the scale of required grid reinforcement and buildout (in building and transport) as well as due to the unavailability of commercially viable alternatives for high-temperature processes (in industry). Therefore, a near and medium-term role for fossil fuels in cooking, transportation, and industry across SSA is unavoidable. Shifting from biomass-based to electric cooking, electrifying the vehicle fleet, and decarbonising industry (while at the same time ensuring industrial growth), will take time and requires a sector-by-sector outlook at the country level.

For instance, at the household scale, liquified petroleum gas (LPG) serves as a realistic near-term alternative to traditional biomass for cooking, offering health benefits and reduced indoor air pollution (Hollada et al 2017). In transport, two- and three-wheelers may embrace electric mobility more swiftly than the personal car sector, which still relies largely on second-hand imports across Africa (UNEP 2020).

In high-emission industries like cement making, carbon capture and storage may emerge as a long-term decarbonisation option given the persistence of process emissions which cannot be avoided by shifting to low-carbon fuels. For steel production, which currently in Africa is predominantly reliant on electrified recycling (World Steel Association 2021), green hydrogen may be adopted as a combustion fuel (Kinch 2022) if a primary steelmaking sector were to burgeon in SSA. The path to decarbonisation of nitrogen fertiliser production involves green hydrogen but will continue relying on natural gas in the near term, especially if domestic production of fertiliser in Africa is to increase—which appears a realistic development objective, given the very low use of fertiliser in most African countries, both per capita and per unit of arable land (World Bank 2022a, 2022b, 2022c).

Assessing the future demand for oil and gas in SSA is thus critical. The role of oil and gas will vary by country, depending on available resources and industrialisation pathways. Different countries are, or may become, hubs for diverse types of goods: Ethiopia might become a prime exporter of agro-processed goods (e.g. textile, leather) thanks to its favourable climate for agriculture and animal husbandry (Okereke et al 2019), whereas Guinea could conceivably become a producer of sponge iron based on its iron ore resources (Sterl et al 2023). The type and structure of investments in industrial development will, accordingly, also differ at the country-level, with some sectors (e.g. steelmaking) being strongly dominated by a few multinationals, and others (cement making, textile processing) more typically driven by local industries (Sterl et al 2023). Overall, the important question is whether the demand for oil and gas for industrialisation in SSA is likely to remain a small fraction of global demand.

Initial scenarios suggest that this may indeed be the case. For instance, (Sterl et al 2023) suggest that under a wide range of potential developments of industrial and economic growth, energy-related emissions from African countries would certainly rise strongly in the coming decades (albeit without emissions per capita ever reaching the levels of today's industrialised world), but then peak around the decade 2040–2050. This holds even under ambitious assumptions of demand growth and industrialisation, as it can be expected that such ambitious development will eventually entail strong end-use electrification alongside a continued deployment of low-carbon electricity generating sources, thus mitigating the emissions impact of continuously rising energy demand.

5. What energy transition means for fossil fuel-dependent economies: what are the opportunities and risks in energy exports from SSA?

Investments in new extraction infrastructure for export may carry risks, such as stranded assets, amid global decarbonisation efforts. Often, debates around SSA countries' efforts to expand oil and gas exploration frame their legitimate desire to earn foreign revenues against the backdrop of global decarbonisation, essentially pitting climate change concerns against equity and development aspirations.

One key perspective to consider is that Africa's historical contribution to global oil and gas production has been relatively modest (Climate Action Tracker 2022). This fact, combined with its relatively low share in unexplored oil and gas reserves and its limited domestic consumption, suggests that SSA is unlikely to 'break the carbon budget' ahead of other, larger producers. The critical question, therefore, is therefore less about whether oil and gas exploration across Africa aligns with global climate goals—recent research already having shown that this is hardly relevant (Sterl et al 2023)—but rather whether oil and gas exploration represent the most promising investment opportunities for Africa amid the backdrop of a world that may succeed in decarbonising (Mulugetta et al 2022).

International organisations like the International Energy Agency (IEA) and the International Renewable Energy Agency (IRENA) have argued that global oil and gas consumption must start declining soon and undergo drastic reductions by mid-century to limit global warming. The IEA has gone so far as to suggest that achieving net-zero objectives necessitates a halt in the development of new oil and gas fields (IEA, n.d.). Major financial institutions like HSBC Bank have also aligned themselves with these climate targets (HBSC 2022). (The same logically applies to coal, but in SSA, coal consumption is dominated by South Africa, which is already planning a coal phase-out (Mirzania et al 2023)).

On a global scale, numerous proposed investments in oil and gas projects that are still under consideration indicate that the industry has yet to fully align itself with the long-term goals of the Paris Agreement. These mixed market signals generate substantial uncertainty about the medium-term viability of new oil and gas infrastructure investments in Africa. While SSA's domestic demand for oil and gas is expected to rise in the short to medium term (Sterl et al 2023), this will not necessarily prevent global demand from falling, exposing the risk that African supply may not be the least-cost option—unless it is focused mostly on catering to domestic supply, as opposed to the export-oriented strategies of various countries in the past.

Recent experiences paint a challenging picture (Mihalyi and Scurfield 2020). Several SSA countries announced commercially exploitable oil and gas discoveries in recent years, but those that reached production by 2020, such as Mauritania, Ghana, and Niger, earned substantially lower revenues than initially forecast. These shortfalls primarily stemmed from production values falling far short of optimistic projections, with Mauritania experiencing revenues as much as 90% lower than expected. Moreover, oil and gas discoveries in several countries, including Sierra Leone and Liberia, proved to be commercially unviable.

Given these uncertainties, SSA countries endowed with oil and gas resources must carefully weigh short- to medium-term opportunities against long-term risks and opportunity costs. The situation is most precarious when the development of fossil resources would take many years, given the volatility of commodity price markets and the time needed to develop alternative economic activities. In such cases, strategic planning that accounts for potential market fluctuations, revenue volatility, and alternative development paths becomes imperative.

With the long-term prospects for oil and gas as revenue-generating commodities declining amid global decarbonisation efforts, SSA countries are exploring alternative options for economic growth. These alternatives, often in parallel with fossil fuel resources, could potentially drive export revenues and foster sustainable development. Two key prospects on the horizon are green hydrogen and critical minerals.

Africa boasts abundant high-quality resources for renewable electricity generation, particularly in regions close to coastlines. The IEA estimates that Africa could produce up to 5000 million tons (Mt) of green hydrogen per year at a competitive cost of less than $2 per kilogram within 200 km of the coast (IEA 2022). Recent analysis by IRENA integrates the option of building electrolysers to produce low-cost green hydrogen from VRE plants in North Africa (IRENA 2023a). According to this analysis, the region could produce up to 24 Mt of hydrogen per year by 2040 at a cost of $2 per kilogram or less.

Green hydrogen, along with its derivatives such as ammonia, holds immense potential for decarbonising heavy industries like steelmaking and fertiliser production. However, the IEA forecasts a gradual uptake of green hydrogen demand worldwide, with its widespread adoption lagging behind other clean energy alternatives. Several factors contribute to this slow start, including the prohibitive transportation costs associated with shipping hydrogen in its pure form and the limited development of major industrial users of green hydrogen within SSA.

Importantly, the economic pathway for hydrogen production may involve manufacturing hydrogen derivatives like ammonia, which can be feasibly transported (Liebreich 2022). Alternatively, African countries could become locations for hydrogen-based production processes (bringing the industry to Africa, instead of the hydrogen to industrialised regions). For instance, countries with iron ore resources, like Guinea, could leverage green hydrogen for sponge iron production, exporting the processed iron to steelmakers in developed nations.

However, it is crucial to acknowledge that several significant economic risks are associated with such megaprojects. Take, for instance, the suggested 30-gigawatt power-to-hydrogen plant in Mauritania, estimated to cost $40 billion—an investment nearly six times Mauritania's entire annual GDP (IRENA 2023a). Careful consideration must be given to who benefits from these massive green hydrogen projects to ensure widely shared prosperity, particularly in the absence of strong institutions (Davis et al 2021).

Africa is already a major supplier of critical minerals essential for electrification and decarbonisation, including cobalt, manganese, and natural graphite, required for battery production. In 2020, Africa accounted for over 30% of global production of these minerals. The continent is also believed to house substantial deposits of other critical minerals such as nickel, vital for the energy transition. The deposits of these minerals are extremely divergent at the country-level, and tend to be concentrated in a few select countries; for instance, nearly all of Africa's current cobalt production comes from the Democratic Republic of the Congo; nearly all of its manganese from South Africa and Ghana; and nearly all of its graphite from Mozambique, Madagascar, Gabon, and Côte d'Ivoire (IEA 2022).

As global demand for these minerals grows with the progress of energy transitions, Africa's contribution to the market becomes increasingly significant. According to the IEA, if Africa maintains its current market share in battery minerals until 2050, total export revenues from these minerals could rival those from fossil fuel exports (IEA 2022). It should be noted that prospects for exploring critical minerals need not only be evoked in the context of replacing lost revenues from fossil fuel exports: for instance, as in the case of coal-dependent South Africa, expanding critical minerals extraction could be an avenue to absorb jobs lost elsewhere in the mining sector against the backdrop of a coal phase-out (Mirzaniah et al 2023).

However, venturing into the critical minerals sector requires careful planning. Supply chains for certain materials, like lithium, may face bottlenecks, and materials currently in high demand may be replaced by superior alternatives in the future (Greim et al 2020). Consequently, global trade in these minerals is susceptible to price shocks similar to those affecting the global gas market and faces risks of stranded assets, given the long lead time for new mining projects.

For countries considering mineral exploration, prudent resource governance is paramount. Sustainable mining practices should be adopted to prevent adverse effects on human rights and the environment. Moreover, ensuring that the minerals value chain substantially benefits the local economy through job creation, innovation, and the export of processed products, such as battery production, is essential. In terms of human resources, efforts to regulate the sector and formalise employment in mining critical minerals should allow better working conditions, fair pay, and reliability and transparency along the supply chains (Byemba 2020, Bamana et al 2021). Simultaneously, research into the environmental footprint of critical minerals mining is needed, particularly in the context of the water-energy-food nexus (Simpson et al 2023).

6. Conclusion: charting sustainable energy transitions in SSA

This synthesis highlights the critical questions that underpin the determination of energy transition pathways for SSA. The current evidence base remains limited, and various disparities and gaps persist. However, our synthesis leads us to the following conclusions:

6.1. Viable buildout of VRE-based electricity systems

In theory, SSA countries should be able to establish cost-effective electricity systems predominantly reliant on VRE. This feasibility, however, hinges on (i) achieving reductions in the cost of capital for VRE technologies through risk mitigation, mobilising substantial financial resources, and (ii) enhancing existing grids to accommodate greater VRE capacity. Existing models often overlook these critical variables and their variations across countries. Some nations already attain low cost-of-capital values, rendering VRE economically competitive compared to fossil fuels; and some already have grids suitable for absorbing substantial amounts of VRE. Others lag due to disparities in attracting financing and due to grid infrastructure limitations. To model the feasibility of high VRE penetration, comprehensive, country-specific, network-level studies coupled with capacity expansion planning studies are imperative.

6.2. Supply, transport and offtake as a package deal

The growth of electricity demand in SSA is constrained not only by supply but also by per-capita income. Despite successful electrification efforts, per capita electricity consumption in SSA will remain significantly below middle-income levels in the near-term. The presence of reliable offtakers of produced electricity is not a given, which means that integrated strategies are essential to couple supply, transport, and consumption of electricity, attracting C&I customers and improving grid services to allow electric utilities to reach good financial health—enabling them to invest in expanding access to high amounts of potential (but low-bill) customers waiting for connections.

6.3. Near-term growth but long-term phase-out for fossil fuels

SSA's economic development across households, transportation, and industrial sectors is expected to necessitate increased fossil fuel consumption in the short term. This demand growth addresses requirements for cooking, mobility, housing, and production. While electrification complemented by renewables is a long-term option for many of these sectors, the transition will require time. Acknowledging the practical limits of clean alternatives in sectors such as cooking, cement production, and transportation is essential. Liquefied Petroleum Gas (LPG) is likely to play a crucial role in transitioning to cleaner cooking methods, gas will continue to be vital in cement production, and road transportation will rely on diesel and gasoline for an extended period. The potential for decarbonisation in specific sectors and countries varies, emphasising the need for sector- and country-specific analyses.

6.4. Sensible planning of export of energy-related commodities

While some SSA countries may derive significant export revenues from oil and gas resources, these prospects face challenges from global decarbonisation trends. Risks associated with potential stranded assets, coupled with emerging opportunities in green hydrogen and critical minerals, necessitate a comprehensive evaluation of alternative revenue sources. Future exports of oil and gas from African countries may be jeopardised by the pace of decarbonisation in developed economies, with data indicating high risks of low returns despite growing demand for oil and gas within SSA. Green hydrogen and critical minerals present (non-exhaustive examples of) viable alternatives for export revenue generation, and international trends suggest their potential attractiveness for the continent. Country-specific scenario analyses are crucial to determine the potential benefits of these opportunities.

In conclusion, there are various imperatives for undertaking additional country-specific analyses to inform energy policy formulation across SSA and avoiding the oversimplified debates that currently prevail due to the aforementioned lack of information. A thorough exploration of the specific context at the national level of each country is essential to provide a holistic understanding of sustainable energy transition pathways across the African continent, in particular its sub-Saharan part. Lessons learnt there can, in turn, provide valuable information for other developing regions in Latin America and Asia facing (part of) the challenges cited above.

Acknowledgments

We gratefully acknowledge funding from the ClimateWorks Foundation, the African Climate Foundation, and the European Climate Foundation.

We are grateful to Bruno Merven (University of Cape Town), Nadia Ouedraogo (UNECA), Philipp Trotter (University of Oxford & Bergische Universität Wuppertal), Thomas Scurfield, Aaron Sayne, Silas Olang, and David Manley (Natural Resource Governance Institute), and Yacob Mulugetta (University College London) for helpful reviews and discussions.

Data availability statement

All data that support the findings of this study are included within the article (and any supplementary files).