Abstract

This study provides a comprehensive assessment of the environmental and economic impacts of climate change on global and regional forests from now through 2200. By integrating the representative concentration pathway (RCP) 2.6 and RCP 8.5 emission scenarios with climate models, a vegetation model, socio-economic scenarios, and a forest economic model, the study explores long run adjustments of both ecosystems and markets to climate change that have not been studied before. The ecological model suggests that global forest productivity increases under RCP 8.5. The overall supply of timber expands faster than demand through the 23rd century lowering timber prices and creating net benefits in the timber sector. Consumers benefit the most from the lower prices but these same low prices tend to damage forest owners, especially in the tropics. Even without a formal sequestration policy, average global forest carbon is projected to increase by 6%–8% by 2100. Under the RCP 2.6, forest carbon remains stable through 2200 but under RCP 8.5 it is simulated to increase by another 8% with a very heterogeneous distribution across world regions. Under both RCPs, global forest area is projected to increase relative to a no-climate change case until 2150, but possibly decline thereafter.

Export citation and abstract BibTeX RIS

Original content from this work may be used under the terms of the Creative Commons Attribution 4.0 license. Any further distribution of this work must maintain attribution to the author(s) and the title of the work, journal citation and DOI.

1. Introduction

There are now many economic studies that examine how climate change may affect forests, forest carbon and ultimately the forestry sector. This literature, with the exception of Favero et al (2018), has investigated the expected impact of climate change just through 2100. By restricting analyses to the 21st century, the literature has been limited to a period where on average forest productivity, forest cover, and forest biomass per hectare all increase. It is not surprising that the literature has come to the conclusion that carbon sequestration and timber supply will increase and timber prices will fall (Perez-Garcia et al 1997, 2002, Sohngen et al 2001, Lee and Lyon 2004, Buongiorno 2015, Tian et al 2016, Favero et al 2018). These studies provide a comprehensive picture of estimated climate change impacts through 2100.

The analysis involves a wide range of economic scenarios, emissions, and climate outcomes in order to provide a comprehensive and integrated perspective on what might happen by 2200. This study explores what may happen to forests beyond 2100 under two extreme emission scenarios: the Representative Concentration Pathway (RCP) 2.6 scenario which will stabilize climate after 2100 and the RCP 8.5 scenario which will drive further increases in global average temperature. Studying potential long-term effects is important to understand what is at stake depending on the emission scenario the world ultimately follows. Understanding specifically how forests may react is important because it is well known that ecosystems are sensitive to temperature. Specifically, long-term analysis is essential to forestry because many timber species are long-lived so the consequences of decisions made this century, will influence carbon and timber supply after 2100. How forests, and the people who manage them, react to either of these two different emission paths is not clear. By assessing ecological and economic impacts further into the future, we can better understand the eventual consequences of choosing different emission paths and the benefits of taking near term mitigation actions to prevent these changes from ever happening.

It is well established that forests are sensitive to climate change. Warmer climates, longer growing seasons, and elevated atmospheric CO2 concentrations can accelerate tree growth (Norby et al 2005, Kirilenko and Sedjo 2007, Sitch et al 2008, Piao et al 2013, Schimel et al 2014). However, increasing frequency and intensity of disturbances (e.g. wildfires, pest outbreaks, wind throw) may compensate stimulating effects and lead to reduced forest biomass storage (Westerling et al 2006, Zhao and Running 2010, Abatzoglou and Williams 2016, Schoennagel et al 2017, McDowell et al 2020). Moreover, warming is likely to cause ecosystems to migrate causing certain forest types to expand locally and others to contract (Bachelet et al 2008, Gonzalez et al 2010). Dynamic global vegetation models (DGVM) are widely used tools to mechanistically simulate climate change impacts on vegetation functioning and structure and to estimate how multiple factors of global environmental change shape future global forests (Bachelet et al 2008, Sitch et al 2008). Combining these ecological effects with an economic model is important because market forces also shape at least managed forestland and consequently carbon storage.

The economic methods in the literature vary greatly. First, some studies focus only on forest productivity and project changes in the yield function for each forest type (Perez-Garcia et al 1997, 2002, Buongiorno 2015) while other studies include also forest disturbance and stock effects from dieback and movements of biomes (Sohngen et al 2001, Lee and Lyon 2004, Tian et al 2016, Favero et al 2018). Second, some studies focus on global estimates while others only on single countries such as the United States (Joyce et al 1995, Sohngen and Mendelsohn 1998, Irland et al 2001, Alig et al 2002, Wear 2011, Beach et al 2015), Europe (Nabuurs et al 2002, Solberg et al 2003, Hanewinkel et al 2013) and others (Aaheim et al 2011, Ochuodho et al 2012). Finally, some analyses use a partial equilibrium approach and assume prices remain constant (Hanewinkel et al 2013), while others take a general equilibrium approach and compute how prices change in response to changes in supply and demand (Sohngen et al 2001, Tian et al 2016, Favero et al 2018).

This study includes productivity changes as well as dieback and spatial shifts in the distribution of ecosystem types into account. The analysis is global in extent with a very detailed description of regional implications. The analysis projects how price changes as a result of change in timber supply and demand in a dynamic framework.

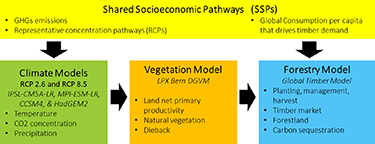

This study follows the logic of an integrated assessment framework (figure 1). The study begins with the moderate and fast growing economic and population projections of the Shared Socioeconomic Pathways (SSPs) (Riahi et al 2017) to calculate global consumption per capita and future greenhouse gas (GHG) emissions. The SSPs were used to predict likely GHG emission scenarios. Simplified Earth system models turn these emission scenarios into RCPs that specify future atmospheric GHG concentrations. The different concentrations in turn lead to different paths of radiative forcing. The radiative forcing gradually warms the oceans leading to changes in climate throughout the planet. We examine the lowest (RCP 2.6) and highest (RCP 8.5) emission scenarios in order to bracket the possible GHG and climate outcomes for the future. Four CMIP5 climate models (IPSL-CM5A-LR, MPI-ESM-LR, CCSM4, and HadGEM2) are used to generate different possible climate outcomes from the RCP 2.6 and RCP 8.5 concentration trajectories. 6 The four models estimate that under the RCP 8.5 scenario, global average temperature increases at a rapid rate through 2150 and then gradually slows, reaching 7 °C–11 °C above 1900 by 2200 depending on the climate model. On the other hand, under the RCP 2.6, global average temperature is projected to stabilize and stay below 2°C by all four climate models (figure S1 is available online at stacks.iop.org/ERL/16/014051/mmedia).

Figure 1. Conceptual diagram.

Download figure:

Standard image High-resolution imageAll the economic scenarios assume continued but declining population growth beyond 2100 with stabilizing population in 2200. The moderate economic scenarios assume continued but declining economic growth rates (figure S2). The SSP5 economic scenario assumes the global economy will grow at 4% indefinitely and it is the only scenario that has growth rate fast enough to generate the RCP 8.5 emission scenario (Riahi et al 2017). We consequently pair the SSP5 growth scenario with the RCP 8.5 emission scenario. We match the SSP1, 2, 4 and 5 scenarios with RCP 2.6. All four growth scenario could lead to emissions pathways in line with RCP 2.6, provided there is sufficient global mitigation (e.g. a rising carbon tax). In order to focus only on climate change impacts, this study does not explore policies designed to store more carbon in forests or use woody biomass for energy production for mitigation, a subject that has been covered elsewhere in the literature (e.g. Sohngen and Mendelsohn 2003, Favero and Mendelsohn 2014, Favero et al 2017, 2020).

The resulting eight climate change projections (two RCP scenarios, four climate models) are used as forcing for the Land surface Processes and eXchanges dynamic global vegetation model LPX-Bern (Stocker et al 2013, Prentice et al 2011, Mendelsohn et al 2016), yielding eight ecosystem change trajectories from the present to year 2300 7 in response to increasing atmospheric CO2 concentrations and changes in climate conditions. In the simulations, increasing CO2 generally stimulates photosynthesis and growth, while limitations by nitrogen availability induce relatively small constraints to the fertilizing effect of CO2 (Stocker et al 2013, Arora et al 2020). Effects of altered precipitation regimes and meteorological droughts lead to a replacement of temperate forests by drought-adapted vegetation of lower stature in today's locations of template forests (e.g. eastern US, Europe, northeastern China).

Figure S3 shows the effects of climate change on forests under the simulations from the four climate models under RCP 2.6 and 8.5. Rising temperatures reduce limitations to the establishment of forests in temperature-limited regions, leading to a general poleward-shift of vegetation zones (biomes) and an expansion of forest area, especially in high northern latitudes. With RCP 8.5, the direction of change is similar across climate models but the extent of change varies. The vegetation model estimates the smallest forest decline under the CCSM4 climate prediction and the largest decline with the HadGEM climate prediction. Moreover, under the CCSM4 climate scenario, the boreal forest in Canada is projected to disappear by 2190 to be replaced by temperate forest. In the tropics, the vegetation model simulates relatively stable forest coverage until 2100. But with three of the four climate change scenarios under RCP 8.5, the tropical forest biome contracts and is replaced by savannah vegetation in western Amazonia by year 2300. HadGEM also predicts a substantial drying of the Amazon Basin which in turn leads to a regional decline of the tropical forest biome. Simulated vegetation changes in Brazil are similar across simulations forced with different climate model outputs and generally suggest a transition to savannah vegetation by 2300 in western Amazonia for all simulations except the one forced by climate models outputs from CCSM4. Under the RCP 2.6, forest area and biome distributions remain largely stable after 2100 although there are a range of predicted effects on temperate forests. Although forests decline in some regions, and transition from type-to-type in others, forest productivity is simulated to increase in general with higher concentrations of CO2 under the RCP 8.5. The increase in productivity simulated in the 21st century continues into the 22nd century albeit at a declining rate of increase. This is linked with a declining sensitivity of photosynthesis to CO2 at high concentrations. The productivity increase in the RCP 8.5 scenario is substantially higher than in the RCP 2.6 scenario. There is dieback associated with the transition from one forest type to another but it tends to have a small effect on global managed forests although it can have a significant effect on regional outcomes (figures S3–S7).

The inputs from the vegetation model and the change in economic growth under each SSP are then included in the Global Timber Model (GTM) (Sohngen et al 2001, 2003, Favero et al 2018) to estimate future planting, management and harvest of managed forestland. This leads to predictions of forest area, forest carbon sequestration, timber supply and demand and overall welfare effects. GTM relies on forward-looking behavior and solves all time periods at the same time; this means that when land owners make decisions today about forest management, they do so by considering future climate change impacts on forests and the implications of their actions today on forests in the future with complete information. GTM is a dynamic economic model of the timber sector. The model solves the optimization problem that maximizes the net welfare of the forestry sector by selecting the harvest of each age class, management intensity, and the area of managed forestland at each moment in time (more information in the SI). The study looks at every scenario from now through 2200 and compares the results to a no climate change (reference) scenario where the economy changes but the climate, and ecosystem functioning and structure do not.

2. Results

2.1. Ecological change

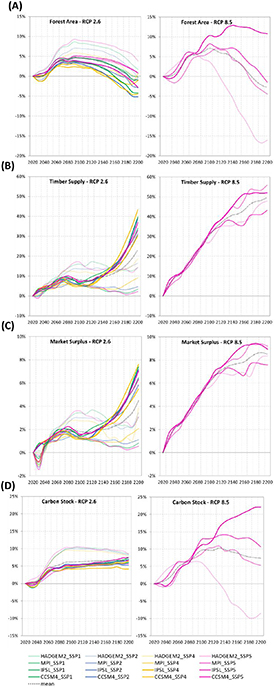

The assumed climate scenarios and corresponding changes in the vegetation, together with market responses drive the projections of areas covered by forests in the future. The modest increase in global temperature associated with RCP 2.6 increases forest area in the 21st century relative to the no climate scenarios. As shown in figure 2(A), this pattern changes in the 22nd century as global forest area is likely to shrink back towards its present level. Under the RCP 8.5 scenario, global forest area is expected to change more than the RCP 2.6 but follow a similar temporal pattern of increasing and then possibly falling. Globally, forest area is simulated to increase on average of 7% and 5% in 2100 and decline by 3% and 1% in 2200 with respect to the no climate change scenario under the RCP 8.5 and RCP 2.6 respectively (mean across simulations forced with different climate).

Figure 2. Estimated change in (A) global forest area, (B) timber supply, (C) net market surplus and (D) forest carbon stock under RCP 2.6 and RCP 8.5 with respect to the reference scenario for each climate and socio-economic scenario (2020–2200).

Download figure:

Standard image High-resolution imageThere is more regional variation in the RCP 8.5 climate projections across climate models which in turn leads to different ecosystem outcomes especially after 2080. Regionally, under the RCP 8.5, Canada is expected to increase forest area the most while by 2200 several countries in both temperate (e.g. Russia and Europe) and tropical (e.g. Brazil and Latin America) areas are likely to experience a contraction in forest area by 2200. Figure 3(A) shows the average of relative change across the four climate models; hence, it does not provide a complete picture of climate effects on regional forests. For example, under the CCSM4 RCP 8.5 projections, LPX projects in Russia a 25% increase of land suitable to be forests in 2300 relative to the present while under the HadGEM RCP 8.5, LPX projects 24% less land suitable for forest in Russia in 2300 relative to today. The future composition of forests is also likely to change significantly, with some species are likely to decline/increase in some regions. The composition will affect management decisions and the economics of the forestry sectors. For example, under the HadGEM RCP 8.5 projections, in Canada total forest area is expected to increase and change its composition shifting from boreal-temperate to temperate-warm temperate. For an economic perspective, this change is particularly important since warm temperate trees (like Southern pine) will grow to maturity at age 30 rather than 60. A similar shift is not expected in Russia.

{kind=link}

{kind=link}

Figure 3. (A) Mean percentage change in regional forest area and (B) mean change in regional forest carbon stock (GtC) under RCP 2.6 and RCP 8.5 with respect to the reference (no climate) scenario in selected years.

Download figure:

Standard image High-resolution image{kind=link}

The projected changes in ecological conditions together with the changes in timber demand are likely to reshape the share of forests that will be managed in the future. Projections of changes in future managed/unmanaged forests follow the projections of total forests: depending on the climate model input, some projections show a decline while others an increase (figure S7). More importantly, the share of managed forests over total forests is likely to be affected by management decisions and climate conditions. For instance, under the same timber demand scenario (SSP5), the share of managed forest over total forest is likely to decline under the climate change simulation with large productivity increases, implying that the timber supply can be met with less managed land. After 2150, it is likely that the productivity increase is not enough and managed forests goes back to the share expected under the no-climate change scenario. Consequently, the share of unmanaged forests is likely to increase under both climate scenarios (figure S8).

Results are very sensitive to the climate model. For instance, under the simulation forces with CCSM4, both managed and natural forests are projected to expand under the RCP 8.5 while under the HadGEM model the expansion will last only until the end of this century and after that both managed and natural forests will be below the no climate scenario. Regionally, under the RCP 8.5 scenario, unmanaged boreal forest in Russia disappears and is partially replaced by managed temperate forest while in Canada unmanaged forest is projected to expand replacing currently managed forest and to change composition from boreal to temperate (figures S9 and S10).

2.2. Global timber market

In the reference (no climate) scenario, the rapid projected increase in global per capita consumption ( in equation (1)) under SSP5 will cause the demand for timber to increase over time by about 2.5 billion m3 yr−1, or more than double, whereas with the more modest growth scenarios (SSP1, 2, and 4) timber consumption increases by 0.2–1.6 billion m3 yr−1 (figure S11). Under these reference scenarios, timber supply increases by increasing management intensity (which increases growth), shifting rotation lengths, altering the mix of species on managed land, and by increasing the area of forest under management.

in equation (1)) under SSP5 will cause the demand for timber to increase over time by about 2.5 billion m3 yr−1, or more than double, whereas with the more modest growth scenarios (SSP1, 2, and 4) timber consumption increases by 0.2–1.6 billion m3 yr−1 (figure S11). Under these reference scenarios, timber supply increases by increasing management intensity (which increases growth), shifting rotation lengths, altering the mix of species on managed land, and by increasing the area of forest under management.

Climate change is projected to cause global timber supply to increase relative to the reference case for each SSP tested (figure 2(B)). That is, of the four indicators examined in figure 2, climate change has the biggest effect on timber supply, causing it to increase steadily over the entire time period. Specifically, industrial wood outputs increase by 8% by 2100 and 23% by 2200 under RCP 2.6 and by 30% by 2100 and by 50% by 2200 under RCP 8.5. These results suggest that the effects of climate change on forest productivity and the corresponding changes of timber supply found by the literature through 2100 (Perez-Garcia et al 1997, 2002, Sohngen et al 2001, Lee and Lyon 2004, Buongiorno 2015, Tian et al 2016, Favero et al 2018) will continue through 2200.

Under both climate scenarios, the largest increases in timber supply are projected to occur in temperate and boreal regions, with smaller changes and possibly even reductions in the tropics. In particular, timber yields are projected to increase significantly under both climate scenarios in temperate areas relative to the no climate scenario as combined effect of changes in vegetation conditions (e.g. warm temperate forests in North regions) and management decisions. On the other hand, there is more uncertainty in the effects of climate change on forest yield in the Tropics under both RCPs (figure S12).

Under RCP 2.6, in 2100, the largest increase in timber supply is projected in Canada (absolute) and in Australia (relative) with only a small reduction in harvesting in Brazil, China and South East Asia. In 2200, the largest increase is projected in Russia (both absolute and relative), the USA (absolute) and Eastern Europe (relative) while the largest reduction is projected in Oceania (absolute) and East Asia (relative). Under the RCP 8.5, in 2100, the largest increase is simulated in Canada and the largest decrease in China. In 2200, the largest increase in relative terms is projected in Oceania and the largest decrease in South American and Sub-Saharan Africa. Results are very sensitive to the climate model output. For example, in the HadGEM2 scenario, the Amazonian tropical forest declines which substantially reduces Brazilian timber supply (figure S13).

Due to rising demand, industrial wood prices rise in all scenarios, but the large global increase in industrial wood supply causes these prices to decline compared to the reference case. With RCP 2.6, expected timber prices fall by 6% in 2100 and 16% in 2200. With RCP 8.5, timber prices fall by 21% in 2100 and by 31% in 2200. The reduction in timber prices in the 21st century is expected to continue through the 22nd century (figure S14).

2.3. Economic welfare

The economic effects of climate change on the forestry sector are measured by the change in the sum of consumer plus producer surplus (net surplus). In the reference scenario, the timber sector has a discounted net surplus of around $351 billion in 2100 and $4 billion in 2200 (discount rate equal to 5%). The simulated increase in ecosystem productivity under climate change leads to an overall increase in net surplus. Welfare in the timber market increases by 2%–6% by 2100 and by 7%–9% by 2200 under climate change scenarios (figure 2(C)). Specifically, under the RCP 2.6, the overall expected discounted welfare gain in 2100 is $7 billion and in 2200, it is $0.2 billion, while under the RCP 8.5 scenario, in 2100 it is equal to $32 billion and in 2200, it is $0.7 billion. Regional variation is significant with a much higher increase in market surplus in temperate areas relative to the tropics. For example, in 2100 the U.S. is projected to increase net surplus by $2 billion and $7 billion while Brazil is projected to decrease net surplus by $0.6 billion and $1.6 billion under the RCP 2.6 and RCP 8.5 respectively (figure S15).

The welfare gain from the increase in forest productivity falls entirely to consumers of wood products. The decline in prices imply consumer can buy more wood products with a lower expenditure. The gain to consumers is distributed across all countries that consume wood products in proportion to their GDP.

On average, timber suppliers around the world end up with lower producer surplus because the increase in productivity in most regions is not enough to offset the lost revenue from lower global prices. However, producers in some regions may gain. For example, producers in Canada, Russia and Europe, are expected to gain welfare over the long-run, especially under the RCP 8.5. This is perhaps surprising given that these regions also experience greater dieback and conversion costs from shifting forest types. But the productivity gains from the replacement of boreal forests by temperate forests outweigh the lower prices and the resulting stock losses. On the other hand, producers in low latitudes (especially Brazil) are likely to experience lower gains in productivity than high latitude countries. That is, they are likely to lose from climate change impacts especially under the RCP 8.5. For example, with RCP 8.5, Brazil likely loses 8% of its average surplus per hectare from 2020 to 2100 and 28% from 2100 to 2200. In contrast, Canada is projected to increase average surplus per hectare by 10% from 2020 to 2100 and by 64% from 2100 to 2200 (figure S16).

2.4. Forest carbon stocks

Interactions between climate change, forested ecosystems, forest management and markets will change the amount of carbon that is stored in forests even if forest owners have no financial incentive to store carbon. Globally, average carbon stocks are projected to increase by 6% under the RCP 2.6 scenario and by 10% under the RCP 8.5 scenario by 2100 (figure 2(D)). After 2150, the expected rate of increase in forest carbon stock (mean) will fall slightly under the RCP 8.5. Moreover, under the RCP 8.5, the expected carbon sequestered in forests vary greatly across climate scenarios especially after 2150 with a maximum increase of 22% and maximum decrease of 9% relative to the reference scenario by 2200. In contrast, under RCP 2.6, forests are projected to increase their carbon sequestration across climate scenarios until 2200. Despite the potential decrease in carbon stock after 2150, the projected carbon sequestered per hectare of forest area is expected to increase under both climate scenarios relative to the reference scenario driven by climate effects and management decisions (figure S17).

Regionally, the largest changes in carbon stocks by 2200 are simulated in boreal areas with Canada projected to increase carbon stocks by 130 GtC (mean) and Russia projected to reduce stocks by 95 GtC (mean) under the RCP 8.5 relative to the reference scenario. The large gains in Canada are driven by temperate and warm temperate forests replacing boreal forests, while the large losses in Russia are driven reduced tree cover. The increase (reduction) in forest area in Canada (Russia) of 63% (30%) relative to the present corresponds to an increase (reduction) in carbon stocks of 90% (35%). Overall tropical forests are projected to experience an increase in forest carbon stock, with some exception in Sub Saharan Africa and South America depending on the climate scenarios. For example, under the HadGEM climate scenario, carbon stock in Brazil is simulated to decline by 8 GtC relative to the no climate scenario in 2200. The RCP 2.6 shows a more uniform distribution of gains in carbon stock across world regions (figure 3(B)).

Finally, by comparing each socio-economic and climate change combination, results suggest that high demand for timber (SSP5) will drive an increasing amount of carbon sequestration in world forests, while the modest economic growth (SSP4) is likely to result in lower carbon sequestration in the future relative to the present values (figure S18). That is, the increase in forest carbon sequestration that is projected to occur over the next two centuries will be the result of both climate and market forces. For instance, under the no climate change scenarios, only SSP5 is likely to see an increase in forest carbon stock far in the future while moderate timber demand under the other SSPs will not be high enough to drive forest carbon sequestration to a level higher than its present status. Additionally, for the same climate scenario (RCP 2.6), the SSP5 drives the highest increase and it increases over time while SSP4 drives the lowest increase. Under the same socio-economic scenario (SSP5), the RCP 8.5 is the one projecting the highest expansion together with the highest uncertainty (figure S19).

3. Conclusions

This study provides a comprehensive and interdisciplinary assessment of the long-term impacts of climate change on the forests through 2200. By extending the analysis to 2200, the study explores long-term adjustments of both ecosystems and markets to climate change that have not been studied before. By focusing on the both high (RCP 8.5) and low (RCP 2.6) emission scenarios and their corresponding socio-economic scenarios, the analysis explores a wide range of outcomes, relevant for forestry through 2200. The results for the 21st century confirm the literature's conclusion that climate change will cause forests to become more productive through 2100 at the global level. For the 21st century, all studies show that global timber supply will increase as the result of an increase in global forest growth, the increasing supply induces lower global timber prices increasing consumers' surplus while decreasing producers' surplus with resulting change in welfare is likely to be positive because the gains to consumer welfare are greater than the losses to producer welfare. After 2100, climate projections, vegetation and market responses through 2200 suggest a larger range of outcomes, especially under the RCP 8.5 scenarios.

Under both RCPs, global forest area is projected to increase relative to the no-climate reference scenario until 2100. After that, there is the possibility of a decline with more than 50% of the scenarios simulated showing forest area below the reference by 2200. Under the same timber demand scenario, climate change is likely to reduce the share of managed forest area because the increase productivity requires less land to meet the demand. Unmanaged forestland will increase and remain higher than the reference case under the RCP 2.6 scenario. Under RCP 8.5, unmanaged forest area will at first increase but then decline possible well below the no climate change levels by 2200. The changes in unmanaged forest area will influence biodiversity and habitat in many ways. We have not explored those nonmarket changes in this paper, but recognize that many of these changes will occur on unmanaged forests.

GTM relies on forward-looking behavior and solves all time periods at the same time; this means that land owners make decisions today about forest management and adaptation actions in anticipation of climate effects. Results show that an incidental by product of climate change adaptation of the timber sector is the increase carbon stock in forests. That is, forest carbon is projected to increase under both RCP 2.6 and RCP 8.5 scenarios even without a formal incentive for forest sequestration in place because of changes in climate conditions and related management decisions. For example, under the RCP 8.5, in 2100 the mean quantity of total carbon stored in forests peaks at 970 GtC (10% more than the no climate change scenario), and then shrinks to 962 GtC by 2200 (current value is about 895 GtC). Even if forest area will decline far in the future, carbon sequestration per hectare is projected to increase.

Finally, behind these results are several assumptions on climate change effects on vegetation and corresponding economic responses to these effects. For instance, in this study we examine one of the lowest representative concentration pathway scenario (RCP 2.6) and the highest scenario (RCP 8.5) in order to bracket the possible GHG and climate outcomes for the future. Future research will explore a wider range of climate scenarios (e.g. RCP 3.4, 4.5 and 6) to better assess the likeliness of these results. Moreover, our results are sensitive to the DGVM used for the study. Underlying results presented here are simulated vegetation changes that suggest a persistently positive effect of rising CO2 on photosynthesis and growth, a simple representation of disturbances (Sitch et al 2003), and relatively mild effects of nitrogen limitation (Stocker et al 2013). Substantial uncertainty surrounds these processes and projected ecosystem changes among a larger set of vegetation models diverge substantially when forced with a specific climate change scenario (Arora et al 2020). Observational evidence suggests a wide-spread tendency towards higher tree mortality and amplified disturbance rates, which is shifting forests to younger and shorter stands already today (McDowell et al 2020). This suggests that the wide-spread increase in timber production projected in this study could be strongly reduced by climate change impacts that are not simulated with high confidence in the vegetation model applied here.

For the economic component of this study, the analysis explores how economic growth will drive the demand for traditional wood and paper products under alternative SSPs. However, carbon mitigation efforts might call for woody biomass to be used as an energy source which would substantially increase wood demand. This may be particularly important to meet stringent emission targets such as RCP 2.6. Mitigation may also encourage timber to replace concrete as a building material. On the other hand, recycling especially of paper might reduce future timber demand. Carbon sequestration may also be an important mitigation tool which would encourage forests to store more carbon (IPCC 2019, Roe et al 2019, Favero et al 2020). These additional demands for timber products and forests are likely to affect our results, the sign of the change and the magnitude is unclear. Finally, both warming and mitigation policies are likely to affect agriculture. The interface between change in timber and agriculture will affect the global and regional demand for land. Future research will integrated climate change impacts on forests and other uses of land together with land-based mitigation actions.

Data availability statement

The data that support the findings of this study are available upon reasonable request from the authors.

Acknowledgments

AF acknowledges the financial support from the Laboratory for Integrated Economics, Engineering, Environment Assessment and Policy, Georgia Tech. The authors appreciate the valuable suggestions from anonymous referees that improved the paper. B.D.S was funded by the Swiss National Science Foundation Grant No. PCEFP2_181115.

Footnotes

- 6

Our analysis does not assign probabilities to scenarios or weights to models.

- 7

This study uses climate and ecosystem projections to 2350 but limit the analysis of the results to 2200. These results are sufficiently far in front of 2350 that they are no longer sensitive to the terminal conditions.