Abstract

The decarbonisation of industry is a bottleneck for the EU's 2050 target of climate neutrality. Replacing fossil fuels with low-carbon electricity is at the core of this challenge; however, the aggregate electrification potential and resulting system-wide CO2 reductions for diverse industrial processes are unknown. Here, we present the results from a comprehensive bottom-up analysis of the energy use in 11 industrial sectors (accounting for 92% of Europe's industry CO2 emissions), and estimate the technological potential for industry electrification in three stages. Seventy-eight per cent of the energy demand is electrifiable with technologies that are already established, while 99% electrification can be achieved with the addition of technologies currently under development. Such a deep electrification reduces CO2 emissions already based on the carbon intensity of today's electricity (∼300 gCO2 kWhel−1). With an increasing decarbonisation of the power sector IEA: 12 gCO2 kWhel−1 in 2050), electrification could cut CO2 emissions by 78%, and almost entirely abate the energy-related CO2 emissions, reducing the industry bottleneck to only residual process emissions. Despite its decarbonisation potential, the extent to which direct electrification will be deployed in industry remains uncertain and depends on the relative cost of electric technologies compared to other low-carbon options.

Export citation and abstract BibTeX RIS

Original content from this work may be used under the terms of the Creative Commons Attribution 4.0 license. Any further distribution of this work must maintain attribution to the author(s) and the title of the work, journal citation and DOI.

Acronyms and abbreviations

| 2DS | 2 °C scenario |

| °C | Degree Celsius |

| CCS/U | Carbon capture and storage/utilisation |

| CO2 | Carbon dioxide |

| COP | Coefficient of performance |

| EAF | Electric arc furnace |

| Efuels | Synthetic electricity-based fuels |

| EJ | Exajoule |

| EPRI | Electric Power Research Institute |

| ETP | Energy Technology Perspective |

| ETS | Emissions Trading System |

| EU | European Union |

| FE | Final energy |

| g | Grams |

| Gt | Gigatonne |

| IEA | International Energy Agency |

| IPCC | Intergovernmental Panel on Climate Change |

| kWhel | Kilowatt hour electricity |

| MVR | Mechanical vapour recompression |

| MW | Megawatt |

| R&D | Research and development |

| St1,2,3 | Stage1,2,3 of electrification |

| TWh | Terawatt hour |

| UE | Useful energy |

| UK | United Kingdom |

1. Introduction

In 2015, industry5 generated 15% (0.5 GtCO2 yr−1) of the European CO2 emissions from fuels combustion, and was responsible for circa 30% (1 GtCO2 yr−1) of the end-sectors emissions, when process and indirect CO2 emissions from electricity and central heat use were included [1, 2]. Fuels combustion provided 70% of the final energy consumed in industry (feedstocks excluded), mostly to supply heat [1, 2]. The remaining 30% was from electricity, which is primarily used for cooling and supplying mechanical power while it plays a minor role in delivering industrial heat [1–3].

Industry is characterised by long-lived capital stocks [4], thus a clear perspective on viable low-carbon options is crucial to avoid further lock-ins into emission intensive infrastructures [5]. In some European countries, coke ovens, blast furnaces, and steam crackers will reach the end of their lifetime or require new investments within the next 10–15 yr [6, 7].

Replacing fossil fuels with low-carbon electricity has become the core climate change mitigation strategy (referred to as electrification, sector coupling, power-to-X or power-to-heat), as supported by many climate change mitigation scenarios [8]. The carbon intensity of electricity has continuously declined in the past decades, at a much faster rate than any other energy carrier [9]. The global renewable energy generation capacity has steadily increased and tapping into this vast energy source would help avoiding the caveats and risks of other options such as carbon capture and storage/utilisation (CCS/U) [10, 11], or carbon dioxide removal [10]. Indirect electrification via synthetic electricity-based fuels (efuels) suffers from low electricity-to-fuel conversion efficiencies, and the requirements of sourcing carbon for the synthesis of hydrocarbons [3, 12]. Although, synthetic fuels are an important complementary low-carbon option when electricity cannot substitute fossil fuels (e.g. chemical feedstocks).

This paper focuses on direct electrification, which makes a more efficient use of electricity as a direct input in electrolytic processes or to supply heat based largely on already mature technologies (e.g. heat pumps, electric boilers and furnaces).

The IPCC [13] lists electrification among the key decarbonisation options for industry, and highlights the lack of robust literature to evaluate its economic, environmental and technological feasibility [13]. Previous studies conducted on the European industry [14–16] estimated the thermal energy demand at different temperature levels and end-uses. While these investigations provide an accurate bottom-up analysis of the heat consumption in industry, they do not focus on electrification. Lechtenböhmer et al [17] investigated the complete electrification of seven manufacturing processes. The study analyses the impact of such scenario on electricity demand, production cost, and emissions reduction in Europe, but it does not provide a complete overview on the viability of power-to-heat in industry. Other studies have discussed electrification of heat from a cross-sectoral perspective [18] or country level [19, 20]. Beyond the European context, Philibert [3] provided a detailed overview of electrification options for industry [3], while Lord [21] presented a series of electrification guides for different manufacturing processes. The EPR [22] used a top-down modelling approach to estimate the potential for industry electrification in the United States. By 2050, nearly 50% of industry's final energy could be electrified when a stringent carbon price is adopted [22]. Mai et al [23] obtained comparable results, i.e. circa 40% electrification by 2050. Khanna et al [24] estimated the CO2-abatement potential of electrification in China, but analysed only four industry sectors and provided results for the aggregated end-use sectors [24].

Thus far, a comprehensive bottom-up analysis of industry energy demand aimed at identifying the achievable level of electrification and its climate change mitigation potential is missing, as well as a clear assessment of the transformations needed at sectoral level. We aim to close these gaps with the present study.

We look at the industry sector in Europe, as here the greenhouse gas emissions regulation is at an advanced stage, and Europe aspires to be a global leader in low carbon technologies. We combine a bottom-up analysis of the energy demand from 11 industry sectors (covering 88% of Europe's industry final energy consumption and 92% of its CO2 emissions) with the assessment of a portfolio of electric technologies implementable in industrial processes. We present three electrification stages, which outline the progressive penetration of electrification in industry, and provide the respective CO2 emissions mitigation potential at different carbon intensities of electricity.

2. Mapping out today's industrial energy use

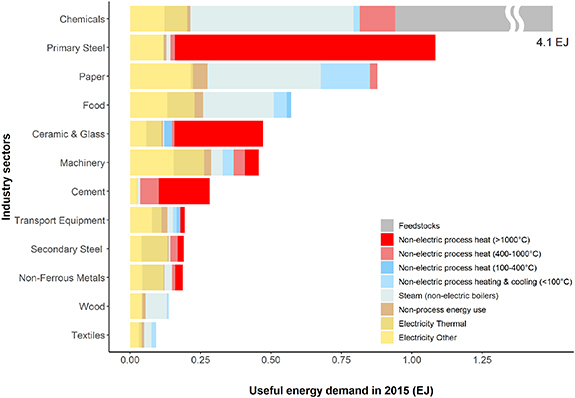

Figure 1 shows the distribution of the UE demand in the selected manufacturing industries examined in this study for 27 EU member states and the United Kingdom (EU27/UK) in 2015 [2] (see supplementary section A.1 Methods (available online at https://stacks.iop.org/ERL/15/124004/mmedia)). FE is the energy available to the end-users (e.g. electricity input for an electric boiler), while UE is the energy output available after the conversion of the FE input through an appliance (e.g. heat output of an electric boiler). While FE is directly measurable, UE is based on sometimes-arbitrary assumptions on efficiency and energy losses. In the present study, the FE-to-UE conversion accounts for all the energy losses occurred within the plant, e.g. steam distribution losses, unrecovered waste heat from processes [25].

Figure 1. Distribution of industry UE demand for the year 2015 in the EU27/UK. See supplementary figure A.1 for a variant of figure 1 without chemical feedstocks and figures A.2 and A.3 for a visualisation of the energy distribution at FE level.

Download figure:

Standard image High-resolution imageThe electricity demand was divided into (1) electricity to supply heating or cooling, i.e. electricity thermal, and (2) electricity used in mechanical power and lighting, i.e. electricity other. Mechanical power was assumed 100% electric. The energy from combustible fuels was divided into non-process energy (e.g. space heating), steam, and thermal energy; the latter was distributed across the temperature spectrum (<100 °C, 100 °C–400 °C, 400 °C–1000 °C, >1000 °C). The non-electric thermal cooling was allocated below 100 °C.

The total UE was 8.7 EJ, which compared to the FE consumption of 13.2 EJ indicates that about one third of the energy input is lost due to inefficiencies and energy losses within the plant. The highest energy consumption is observed in chemicals, primary steel and paper industries, which combined account for 70% of the total UE demand (6.1 EJ). Chemical feedstocks, i.e. fossil fuels used as raw materials, amount to 36% of the total UE (according to their energy content, 3.2 EJ). Nineteen per cent of UE is consumed as electricity (1.6 EJ) and 45% (3.9 EJ) as heat (6% at temperatures below 100 °C, 17% between 100 °C–400 °C, 4% between 400 °C–1000 °C, and 18% above 1000 °C), which leaves great potential for the electrification of industrial processes (see supplementary section A.1 Methods and table A.2).

3. Portfolio of available electrification technologies

Table 1 presents a portfolio of technologies that can substitute the traditional fired-systems for electrifying industrial heat and cooling demand. These technologies lay the foundation for the three electrification stages discussed in the following section and are classified based on technological maturity, achievable temperatures, applications and efficiency [3, 18, 21, 26–28]. The supplementary section A.3 provides a technical description of these technologies and their applications.

Table 1. Electrically powered technologies for industry electrification. Efficiency is the ratio between UE output and FE input of an appliance. The COP measures the heat output (for heat pumps) or the heat absorbed (for chillers) per unit of work input [18–52].

|

Electrically powered technologies can cover the whole temperature spectrum relevant to industrial thermal processes (up to 20 000 °C [53]), and are already established in industry. The applications at low and medium temperature are not sector-specific, consequently electric boilers and heat pumps could be implemented transversally across industry to supply cooling and heat. On the other hand, high temperature processes are highly heterogeneous and require different heating systems, e.g. induction, resistance.

The substitution of fired systems with electrically powered technologies can lead to lower energy consumption as the latter operate with higher or comparable efficiencies [3, 18, 21]. For instance, compression heat pumps use less energy per unit of heat output than any type of boiler and can transfer energy from external heat sources or waste heat, reaching COP above 2 [18, 28].

Despite the many advantages, the extent to which direct electrification will be deployed in industry remains uncertain and depends on the relative cost of electric technologies compared to other low-carbon options [54]. To the best knowledge of the authors, a comprehensive cost analysis of industrial electrification technologies is not available in the open literature. Material Economics [6] analysed the CO2 abatement cost for industry decarbonisation pathways, but aggregated the cost of direct electrification with that of other low-carbon measures, which makes it difficult to put a price tag on a specific technology [6]. An accurate estimate of the electrification costs for industry is particularly challenging due to the heterogeneity of the technologies and processes in use. In many cases, costs are not disclosed by manufacturers, or not available for technologies that are still under development. When investment and operation & maintenance costs are available, they are often applicable to a limited range of heating capacities lower than those used in industry. An exception to this trend is represented by boilers and heat pumps, for which detailed cost analyses have been performed, mostly in the context of residential heating electrification [55]. The overall cost of boilers and heat pumps is driven by the fuel/electricity price [55–59]. Since the price of electricity is three times higher than that of natural gas, the application of electrically powered technologies is often limited to small production volumes [3, 17, 23, 26].

4. Three stages for industry electrification

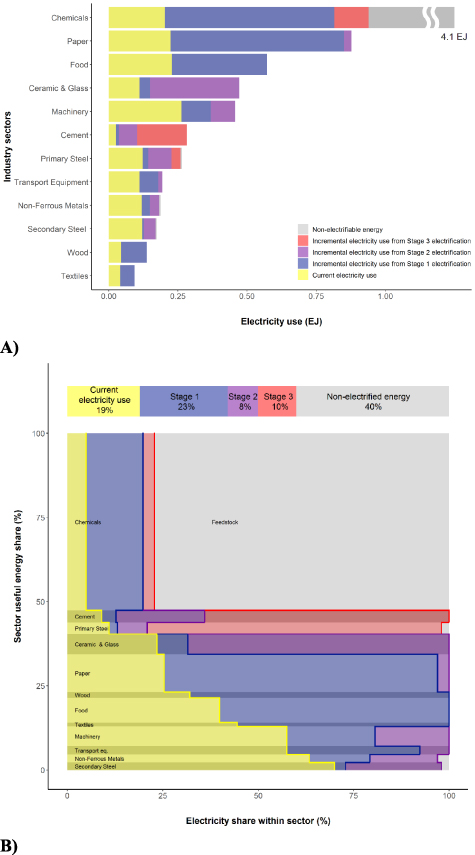

Here we present three electrification stages and aggregate the resulting electrification potential of the European industry. The three stages constitute the potential advancement of industry electrification from status-quo to full electrification, based on the level of complexity of the processes and maturity of the technologies involved. The results are shown in figure 2.

Figure 2. Electrification potential of the European industry; yellow bars: current electricity use; blue bars: incremental electricity use from St1 electrification; purple bars: incremental electricity use from St2 electrification; red bars: incremental electricity use from St3 electrification. Figure 2(A) shows the absolute values of electricity use in EJ, while figure 2(b) the electricity share over UE demand in percentages. See also supplementary figures A.4, A.5, and A.6 for the electrification maps at each stage, and figure A.7 for a variant of figure 2 without the chemical feedstocks.

Download figure:

Standard image High-resolution imageSt1 includes thermal processes that are common to all industries and are therefore considered potential entry points for electrification, as the broad implementation of electric technologies will benefit from the transfer of experience and know-how across the sectors.

St2 corresponds to the more technologically advanced phase of electrification, in which a diverse range of processes and sector-specific technologies are involved. The technologies implemented in St2 vary in heating systems and technical properties depending on products and applications. For this reason, it is expected that electrification will be slower and require a more substantial technological upgrade than in St1.

St1 and St2 involve technologies that are already fully developed and established in industry. On the other side, St3 explores the maximum achievable electrification potential if also technologies that have higher uncertainties and lower technological maturity are included.

In the interest of conceptual clarity, we assume scale and sectoral shares in industrial UE constant at 2015 levels.

4.1. Stage 1—Entry points for industry electrification with mature technologies

The aggregated electrification potential of St1 (blue bars in figure 2) amounts to 42% of the industrial UE demand (3.6 EJ), and 66% if the energy content in chemical feedstocks is not accounted for. The electricity demand from industry doubles when low and medium temperature processes are fully electrified.

At this stage, the energy demand for cooling, space heating, steam generation, and drying, i.e. processes operated at low and medium temperature, is fully electrifiable with compression heat pumps, chillers, MVR, electric boilers, infrared, microwave, and radiofrequency heaters. Such technologies are fully developed and have sufficient capacities for industrial applications (see supplementary section A.3).

Excluding chemicals, cement, and steel, the remaining sectors, which together account for 35% of the industry's UE demand and 40% of its CO2 emissions, can be fully or extensively electrified in St1. Food, wood and textiles are 100% electrified as they mostly require heat below 400 °C [31, 40, 60, 61]. Similarly, paper requires 97% heat below 400 °C [33, 60], while the remaining 3% is consumed in limekilns for limestone calcination during the pulping process (see St2) [33, 60].

Chemicals, steel and cement, which are also the most CO2-intensive sectors, are not easily electrified in St1. Among these, the chemical sector has the largest electrification potential as it primarily consumes energy for cooling and steam. The latter in particular is largely used in steam cracking and reforming, which also require the combustion of fuels for heat supply (see St3) [32, 34].

4.2. Stage 2—A more technologically advanced phase of industry electrification

Overall, the electrified energy in St2 (purple bars in figure 2) is estimated at 50% of the UE demand, i.e. 4.3 EJ (including the 42% from St1), and at 78% when feedstocks are excluded.

St2 involves technologies that are already established in industry and can supply heat above 400 °C. The electrification at this stage mostly relies on electric furnaces with various heating systems and designs. Resistance heating is used for firing ceramics, glass melting, annealing and tempering [37, 62]. Induction, resistance, and arc furnaces are already used for melting, smelting, and refining various metals [26, 48]. Metals used for the production of machinery and transport equipment are also subject to thermal treatments that can be electrically powered [26, 38]. Electric kilns can also be used for calcination, although fired rotary calciners are normally used in industry [63] (see supplementary section A.3).

In St2, paper, ceramics & glass, machinery and transport equipment industries are 100% electrified. Non-ferrous metals and secondary steel have an electrification potential of 97% and 98% of the UE demand, respectively. The remaining energy share represents the usage of carbon-bearing reducing agents used for metallurgical purposes, e.g. smelting and refining [48].

Similarly to what observed in St1, chemicals, primary steel, and cement cannot be extensively electrified with currently available technologies in St2. Chemicals maintain the same electrification of St1, while only re-heating and annealing are electrified in primary steel (see St3). Cement has an electrification potential of 36% of the UE demand that includes the calcination of limestone, whereas the energy for clinker burning is excluded (see St3). Electrolysis of limestone could substitute fired or electric furnaces for calcination, but it is not discussed here due its early stage of development [64].

St1 and St2 rely on technologies that are already used in industry, thus these stages could be implemented simultaneously, potentially accelerating industry electrification. For instance, it may be possible to implement electric boilers for steam production (St1) in parallel with the electrification of metals melting (St2). While all the industry sectors consume steam and could benefit from the installation of electric boilers, metals melting is a more complex process that is operated in selected industries and requires different heating systems, operating conditions etc (see supplementary section A.3). The technical improvement, scaling-up, and integration of electric technologies in St2 is considered more technically challenging than in St1, yet St2 should not be considered a follow-up to St1, nor is the complete electrification in St1 a pre-requisite for electrification in St2.

4.3. Stage 3—Maximum potential of industry electrification with high technological uncertainty

When including technologies with low technological maturity and high uncertainty in chemicals, cement, and steel, the maximum electrification potential increases to 60% of the UE demand (4.7 EJ) in St3 (red bars in figure 2). The remaining 40% cannot be supplied directly with electricity because fossil fuels are used for metallurgical purposes in non-ferrous metals and EAFs, and as chemical feedstocks. When feedstocks are excluded, 99% of the cooling and heat demand from industry can be electrified.

Around 3% of the UE demand from the chemical sector is required to supply heat during steam cracking and reforming. Electric steam crackers and reformers are not established in chemicals production and are considered to have a high uncertainty because they are still at the R&D stage [65, 66]. If these technologies were to be implemented, the total electrification potential of the chemical sector would correspond to 23% of the UE demand, i.e. 20% in St1 plus 3% in St3.

Clinker burning is responsible for 64% of the UE demand from the cement sector and is operated at 1450 °C in large rotary kilns with production volumes of 3000–10 000 tonnes day−1 [63]. The CemZero project is investigating the electrification of cement via thermal plasma. Despite being still at R&D stage, the first results have shown that the process is technically feasible and the investors are looking at building a pilot plant [3, 67]. Existing plasma generators operate at low heating capacity (maximum 7 MW [6]), therefore their scalability to the levels required for cement production (up to 100 MW and above [63]) is highly uncertain.

There are currently three possible electrification routes for the steel industry. (1) Hydrogen can be used as reducing agent for iron, which—to the extent that hydrogen is produced via electrolysis (green hydrogen)—constitutes an indirect form of electrification [3]. This technology has been successfully proven but to date it counts on a single commercial application [21]. Since this study focuses on direct electrification, we exclude hydrogen reduction from our analysis. (2) The electrolytic reduction of iron (electrowinning) could be an option for the electrification of primary steel although it has been demonstrated only at pilot scale [3]. (3) The manufacture of secondary steel via EAF is already well-established and accounts for 40% of the European steel production [68]. On top of the high technological maturity, secondary steel demands from a quarter to a fifth of the energy needed in blast furnaces coupled with basic oxygen furnaces [69]. For these reasons, in St3 we consider the entire substitution of primary steel with secondary steel (EAF + 100% scrap) [69]. This leads to a reduction of primary steel UE demand by 76% (i.e. from 1.1 to 0.3 EJ) compared to St1 and St2, and an electrification potential of 98%. The remaining UE is for coke or coal added for metallurgical purposes [49].

The electrification of primary steel via EAF + 100% scrap is included in St3 due to the high uncertainty of scaling-up the production to current consumption levels, which may be challenging since scrap has already high recycling rates (∼85%) [6]. Higher scrap availability could be achieved with a better management of the accumulated in-use steel stocks, e.g. maximising the recycling rate, increasing the products lifetime or decreasing steel consumption in transport and construction sectors [6, 70]. Some studies have shown that under the saturation of per capita steel stocks in Europe, sufficient scrap would be accessible to meet the total steel demand by the 2050s [6].

Despite the great decarbonisation potential provided by a fully circular steel cycle, the transition from primary to secondary steel is likely to happen gradually. It is fundamental to identify viable low-carbon options for primary steel that can be implemented in the next 10–20 yr to complement the increasing production of secondary steel. The electrification of blast furnaces would provide only a partial reduction of CO2 emissions, since large amounts of coke are required for smelting iron ores [49]. Thus, investments should foster the technical development and industrial application of iron reduction via electrowinning or green hydrogen.

5. The CO2 reduction potential of industry electrification

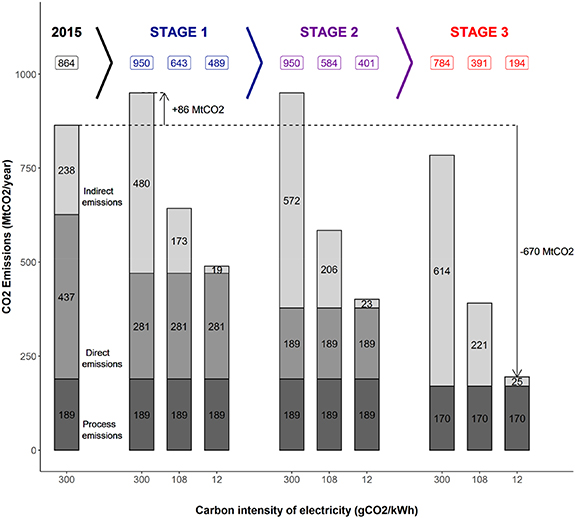

Figure 3 shows the mitigation potential of the aggregated industry sector based on a low-carbon power sector transition within the next 10–20 yr. For each electrification stage, the CO2 emissions from industry are shown for decreasing electricity carbon intensities: 300 gCO2 kWhel−1 is the European electricity carbon intensity in 2015, while 108 and 12 gCO2 kWhel−1 correspond to the IEA 2 °C scenario (2DS) in 2030 and 2050, respectively [1, 71].

Figure 3. CO2 reduction potential of industry electrification in 2015 under St1, St2, St3, calculated at the following carbon intensities of electricity: 300, 108 and 12 gCO2 kWhel−1. See also supplementary figure A.8 for a variant of figure 3 without process emissions.

Download figure:

Standard image High-resolution imageThe substitution of fired systems with electric technologies is associated with an efficiency gain, which corresponds to a decrease of the FE input by 20% in St3 (i.e. from 13.2 to 10.6 EJ). The major energy saving is observed in primary steel, where the FE input is reduced by 79% (i.e. from 2.0 to 0.4 EJ) (see A.1 Methods).

In 2015, the selected industry sectors accounted for 864 MtCO2, of which 50% are direct emissions from fuels combustion, 28% indirect emissions from electricity generation, and 22% process emissions generated by the chemical transformation of raw materials consumed for non-energy use (e.g. limestone calcination in cement manufacturing) [17]. These figures show that the reduction of direct emissions could be the real game changer for the decarbonisation of industry.

In absence of further decarbonisation of power supply, electrifying industry can lead to an increase of CO2 emissions. In St1, the CO2 emissions increase by 10% (950 MtCO2) with 2015 electricity carbon intensity, whereas a deep electrification in St3 would slightly reduce emissions by 9% (784 MtCO2). This is mostly due to the significant reduction of FE consumption from steel in St3, and shows that substituting primary with secondary steel could lower the emissions from this sector already with an unchanged electricity mix. While our electrification stages are largely based on the maturity of electric technologies, these data suggest another approach to industry electrification, which prioritises technologies and sectors with large decarbonisation potential despite a higher uncertainty of viability.

In St1 and St2, which are partially electrified and characterised by a higher FE input than St3, CO2 mitigation via electrification is achieved with breakeven carbon intensities of electricity of 246 and 255 gCO2 kWhel−1, respectively. Between 2000 and 2015, the carbon intensity of electricity in the EU27/UK has seen a steady decrease and if the rate remains constant, ∼230 gCO2 kWhel−1 electricity could be achieved by 2030 [72]. This is significantly less ambitious than the IEA 2DS (108 gCO2 kWhel−1), and suggests that in the next 10 yr a partially electrified industry could be decarbonised even without the implementation of stringent climate policies.

If the power sector is transformed as well (IEA 2DS in 2050: 12 gCO2 kWhel−1), electrification along the three stages increasingly reduces CO2 emissions by up to 78% in St3 (194 MtCO2).

Our analysis implicitly assumes the usage of grid electricity, although industry electrification could also stimulate the expansion of onsite renewable electricity generation. A decentralised renewable energy supply system would not only guarantee greater energy autonomy for industrial plants, but it could also reduce indirect CO2 emissions from electrification [73].

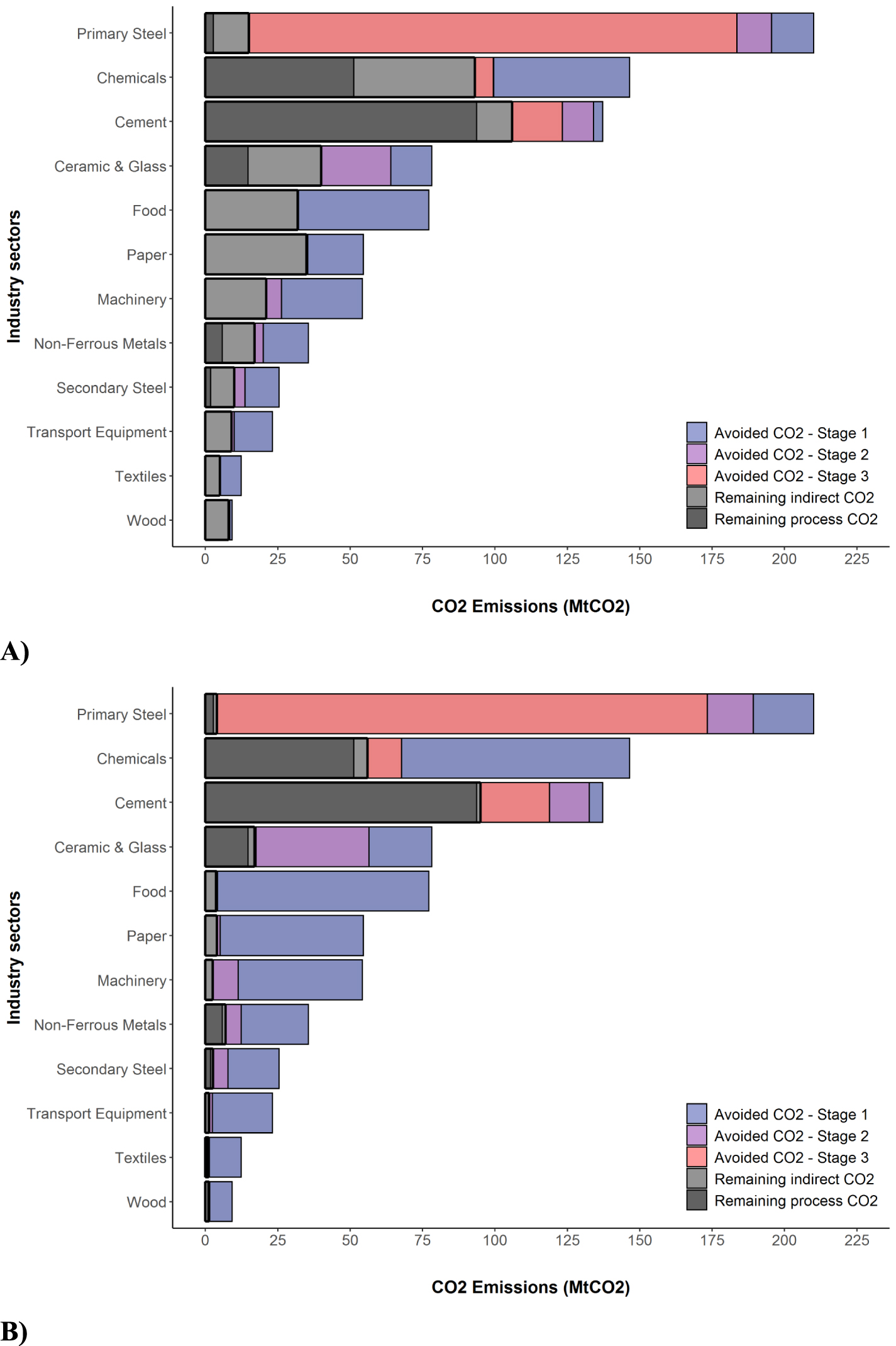

Figure 4 shows the residual and avoided CO2 emissions at sectoral level under a transformed power sector.

Figure 4. Residual and avoided CO2 emissions of the disaggregated industry sector at 108 gCO2 kWhel−1 (figure 4(a)) and 12 gCO2 kWhel−1 (figure 4(b)). The blue, purple and red bars represent the CO2 emissions avoided via electrification in St1, St2 and St3, respectively. The grey bars indicate the remaining process (dark grey) and indirect emissions (light grey). In St3, the only combustible fuels consumed in industry are for metallurgical purposes, thus their CO2 is part of the process emissions. See also supplementary figure A.9 for a variant of figure 4 without process emissions.

Download figure:

Standard image High-resolution imageAt carbon intensity of 108 gCO2 kWhel−1 (figure 4(a)), a partial electrification (St1) reduces emissions by 26% (643 MtCO2). The CO2 emissions from less carbon intensive sectors like food, textiles, machinery, and transport equipment are halved or even more extensively reduced. Advancing electrification (St2) reduces emissions by an additional 7% (584 MtCO2).

The CO2 mitigation in cement, steel and chemicals in St2 is limited by their reduced electrification potential and the large share of process CO2. A deep electrification in St3 significantly lowers the emissions from these sectors, particularly those from primary steel, and halves the overall industry emissions by 55% (391 MtCO2).

At 12 gCO2 kWhel−1 (figure 4(b)), the avoided CO2 emissions further increase from 43% in St1 (489 MtCO2), to 78% in St3 (194 MtCO2). Considering that 87% of the remaining emissions (170 MtCO2) are process related, mostly from cement (48%, 94 MtCO2) and chemicals (26%, 51 MtCO2), electrification alone could almost entirely abate the carbon emissions from cooling and heat demand in industry by 2050 (i.e. 63% of FE).

Power-to-heat cannot mitigate process emissions as they are non-energy related and require a different abatement strategy. This adds another layer of complexity in the development of a CO2 mitigation plan for industry.

6. Industry electrification and the European Green Deal

Reaching carbon neutrality by 2050, as proposed by the European Commission [74] translates into deep CO2 emissions reduction in industry. Re-investing in long-lived fossil-based technologies might lead to carbon lock-in with significant CO2 costs (e.g. through the EU Emissions Trading System (EU-ETS)) or stranded assets, jeopardising the EU climate targets [5]. Industry stakeholders and policy makers should implement a transformation strategy where new investments are directed towards viable technologies with a CO2 mitigation potential.

Based on a comprehensive bottom-up analysis of 11 industrial sectors, we analysed the technical potential for industry electrification and show that electrification could almost entirely abate the energy-related CO2 emissions from industry. Seventy eight per cent of the energy demand is electrifiable with technologies that are already established (St2), while 99% electrification can be achieved with technologies currently under development (St3). Such a deep electrification reduces final energy consumption by 20% (figure 5(a)) and reduces CO2 emissions by 9% already based on today's electricity mix (∼300 gCO2 kWhel−1). With an increasing decarbonisation of power supply (IEA: 12 gCO2 kWhel−1 in 2050), 78% electrification could halve industrial CO2 emissions (figure 5(b)), while a deeper electrification in St3 could cut emissions by 78%, reducing the industry bottleneck to residual process CO2, mostly from cement and chemicals. These findings are based on a technological assessment of electric technologies, however a detailed cost analysis is needed to prove the economic viability of industry electrification.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

Figure 5. Industry FE consumption (figure 5(a)) and CO2 emissions (figure 5(b)) before and after electrification in St1, St2 and St3, at electricity carbon intensity of 12 gCO2 kWhel−1. The percentages of FE consumption and CO2 emissions from industry in the EU27/UK are calculated over the FE and CO2 from the other end-use sectors (transport, residential, services, agriculture and forestry), and from the industry sectors that are not included in our analysis [2]. The CO2 emissions include those from the generation of electricity in the power sector, which are allocated to each end-use sector based on the respective electricity consumption [2].

Download figure:

Standard image High-resolution image{kind=link}

The less CO2-intensive sectors (e.g. paper, wood, textiles etc), which combined account for 40% of Europe's industrial emissions, can be nearly entirely electrified in St2 reducing by 36% industrial emissions. These sectors mostly use low and medium temperature processes, which constitute potential entry points for electrification with established technologies such as electric boilers and heat pumps. These technologies allow for a gradual transformation since existing machines can be retrofitted, or hybrid systems can be installed, e.g. gas/electric boiler [75]. In this way, operators can get used to new technologies maintaining a stable production. Moreover, hybrid systems could ensure a smooth phase-in of electricity benefitting from (1) low electricity price hours, and (2) reduced risks associated with fuels price fluctuations and increasing CO2 prices [3]. These drivers are likely to eventually shift hybrid operations towards all-electric systems.

The analysis shows that the most CO2-intensive sectors, i.e. primary steel, chemicals and cement, are the most challenging to electrify.

The energy demand from the cement sector could be fully electrified via power-to-heat, nevertheless the scalability of new technologies remains a critical aspect. In this sector, the CO2 abatement potential of electrification (31%) is limited due to the large share of process CO2 (68%), which can be reduced via CCS, or with alternative raw materials [76].

The heat and cooling demand from the chemical industry can be 100% electrified, although when the energy contained in feedstocks is accounted for, the electrification potential reduces to 23%. This electrification level can cut 62% of the sector CO2 emissions, however end-of-life emissions are not comprised in the calculation. Indirect electrification is likely to play a complementary role to direct electrification in the reduction of CO2 emissions from the chemical industry. High production volume chemicals can be synthesised with green hydrogen from electrolysis [3]. However, the synthesis of hydrocarbons relies on the implementation of CO2 capture or other methodologies to source non-fossil carbon (e.g. direct air capture or biomass) [3, 77]. Synthetic fuels like bio-naphtha can also be produced from biomass [6, 78, 79].

The electrification of steel via EAF + 100% scrap feed could reduce the energy consumption from this sector by 70% and the CO2 emissions by 74%. Electrowinning and hydrogen-based reduction of iron are the most advanced routes for electrifying primary steel, and could prevent the usage of coke and CCS/U [3].

The complete electrification of industry requires two to three times more electricity (1786–2313 TWh) than the sector currently uses. In 2017, the renewable energy production capacity in Europe was nearly 1000 TWh [54], i.e. circa half of that required to meet the demand from industry electrification in St3. The generation capacity will have to increase by 40 TWh per yr until 2050 to meet the electricity demand in St3 [54]. An ongoing expansion of carbon-free power is a prerequisite for reducing emissions via electrification. This includes overcoming the economic and technical challenges of integrating high shares of renewables with distribution and transmission grid enhancements and storage technologies. Many modelling studies show that 100% renewables based energy systems can be technically and economically viable [80–84], however the expansion rate and the large upfront capital expenditures required for such disruptive transformation constitute significant barriers [85, 86].

An extensive electrification of industry will intensify the electricity peak demand and affect the energy costs since electricity prices tend to be higher in peak hours. Industry will have to maximise its demand flexibility and develop new smart approaches to peak-load management. Load shifting can be achieved by implementing storage technologies (e.g. batteries and renewable-gas storage), or by installing hybrid technologies, which allow switching from electricity to gas depending on the prices, and integrating renewable electricity from wind and solar power when available [87]. Another option is to increase onsite electricity generation that would provide greater autonomy and lower risks due to price volatility [73]. Circa 40% of the electricity consumed in industry is self-generated, of which only one fourth is produced from renewables [73]. Electrification could stimulate the expansion of decentralised energy supply systems as well as the integration of larger shares of renewable power.

The electrification of industry implies significant changes in production processes and is often met by industry stakeholders with scepticism. In most European countries, powering industrial systems with electricity would lead to an increase of the production cost since electricity is on average three times more expensive than natural gas [88]. An evident case concerns electric furnaces or heat pumps that have been narrowly adopted despite their technological maturity. In turn, the limited number of demonstrative applications as well as the lack of proven systems at large scale, hinders the further development of electrically powered technologies and the progress via learning-by-doing. Industry investments in electrification, not only monetary but also for the acquisition of technical expertise will probably stall until a clear scenario is presented where electricity is going to be cost-competitive.

Transformative investment decisions require economic incentives and appropriate policies; here we identified three pillars to support the electrification of industry. First, the reduction of electricity taxation and levies to create a level playing field across energy carriers and a competitive electricity price. The results of such action can be observed in Sweden, where the difference between electricity and gas price is almost half than the European average [88], and industry is leading very ambitious projects to electrify steel and cement [3]. Second, the reduction of investment uncertainties by creating a clear carbon price signal for industry possible by complementing the EU-ETS with a minimum price, while reducing the carbon leakage risk for those sectors that face non-EU competition [89]. Third, the establishment of complementing policies such as technology support schemes and market introduction programs where carbon price fails to incentivise investments [89]. Catalysed by an advancing policy environment, industry can make efficient use of low-carbon electricity. Technologies available today provide entry points towards a deep electrification and first moving companies can benefit from emerging markets for low-carbon products.

Acknowledgments

The research leading to these results has received funding by the Australian Department of Foreign Affairs and Trade and the German Federal Ministry of Education and Research (BMBF) under the grant agreement No. 03EK3046A (START Project) and from the European Union's Horizon 2020 research and innovation programme under grant agreements No. 821124 (NAVIGATE) and No. 730403 (INNOPATHS).

Data availability statement

The data that support the findings of this study are available upon reasonable request from the authors.

Footnotes

- 5

In the Introduction, industry includes manufacturing sectors, mining, construction, coke ovens and blast furnaces [2], while in the following sections, unless otherwise noted, industry refers to the selected sectors analysed in this study (see supplementary section A.1 Methods).